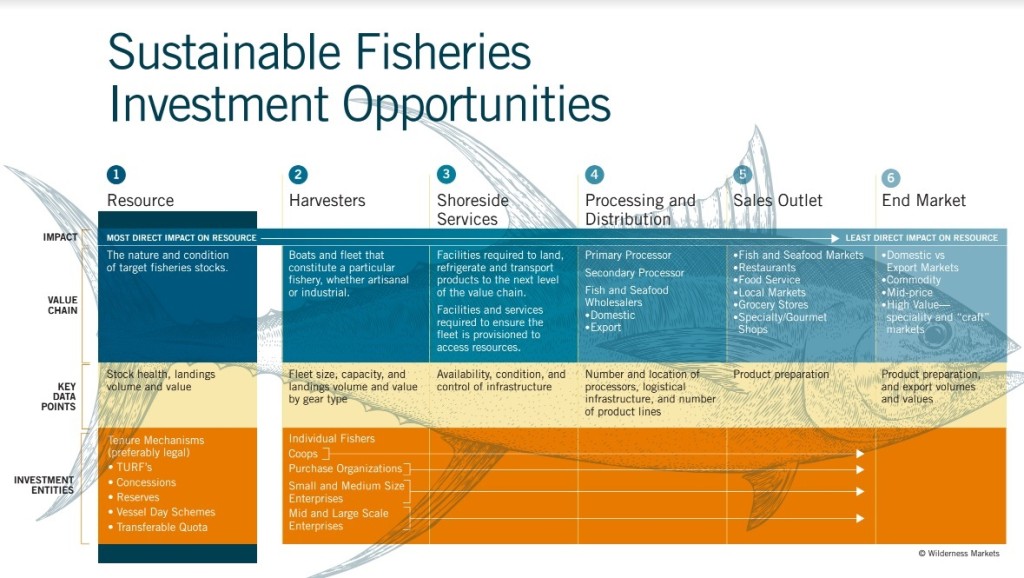

Why we are helping to setting up a harvester cooperative in Indonesia’s blue swimming crab fishery

Wilderness Markets, in collaboration with Blue Star Foods (USA), PT Blue Star Nusantara through one of its subsidiaries PT Siger Jaya Abadi, recently teamed up to assist in the formation of a harvester cooperative in Indonesia. We were recently honored to participate in the launch of the cooperative in Maringgai.

Based on our experience in coffee, cocoa, tea, cashew, macadamia and honey value chains, we have plenty of experience on the advantages and disadvantages of working with producer organizations (POs), usually cooperatives (1). They often fail, riven by poor management, member disagreement and poor financials. Indeed, Dalberg (2) attributes some of the main reasons for lack of smallholder participation to one or more of the following reasons:

Based on our experience in coffee, cocoa, tea, cashew, macadamia and honey value chains, we have plenty of experience on the advantages and disadvantages of working with producer organizations (POs), usually cooperatives (1). They often fail, riven by poor management, member disagreement and poor financials. Indeed, Dalberg (2) attributes some of the main reasons for lack of smallholder participation to one or more of the following reasons:

- POs provide poor services because of low internal capacity

- Insufficient access to resources like financing and technical assistance

- Exclusion of smallholders and women from POs

- Weak governance and leadership of the PO

- State intervention in POs for political gain

So why did we decide to support this initiative?

- Improve harvester representation in the fishery: Many of the harvesters in this fishery are unregistered individuals, with limited access to services and no mechanism for representation

- Secure access to technical assistance for harvesters for best fishing practices

- Create access to financing for harvesters to support their transition to more sustainable fishing methods to decrease pressure on the fishery

- Improve economies of scale: Developing an aggregation mechanism like a PO to permit harvester participation in a global value chain on key issues such as price, quantity and standards.

1. Improve Harvester Representation

Field research in the fishery indicated low levels of harvester registration via the national fisher identification card (Kartu Nelayan). Therefore, these individuals are unable to access a range of government services.

At the same time, the Government of Indonesia has established benefits for cooperative structures to effectively serve its population; however, by not having a cooperative structure in place the harvesters are unable to access these services.

2. Secure Access to Technical Assistance

In addition to government assistance, strong opportunities exist for other value chain stakeholders to provide technical assistance and financing for harvesters. Working closely with Blue Star Foods and its subsidiaries, primarily around reducing environmental impacts and improving harvest value, Wilderness Markets has identified a series of technical assistance measures that Blue Star Foods has committed to supporting. These include access to improved pricing, changes in gear to address the ecosystem impacts of gill nets and increasing access to cold storage and ice to improve product quality.

3. Create Access to Financing

Extensive interviews with a range of national and international banks focused on supporting producer organizations revealed considerable barriers to participating in this sector. These included the lack of individual registration, the lack of payment and history records and the lack of harvester aggregation. Furthermore, most banks stated a preference for at least three years’ worth of records and transaction history for producer organizations.

4. Improve Economies of Scale

While harvesters have historically been able to access markets at the collector or mini-plant picking stations, they have done so at a significant disadvantage to their financial interests. Historically, this may not have been an issue to the remainder of the value chain, but increasing concerns regarding quality and sustainability are resulting in a greater focus on the role of mini-plants and their relationships with harvesters. In the blue swimming crab fishery in Indonesia, where over 90% of production is exported into an increasingly global and competitive market, the value chain can no longer afford to ignore the harvesters and if the harvesters are to remain competitive, they must increase their participation.

“In fact production organized based on GVCs [Global Value Chains] and production networks, governed in part through the use of standards, has increased the need for farmers to be organized in order to be included in modern market trade.” –Dr. Eva Csaky, 2014 (3)

A final consideration relates to equity. Across a range of fisheries Wilderness Markets has evaluated, there is a striking lack of any formal organization to represent harvester’s own interests, to aggregate services and access value chains. This has, more often than not, resulted in harvesters being “price takers” for their efforts, while financial benefits have aggregated in the middle of the supply chain.

Conclusion

Wilderness Markets is only too aware of the failure rate associated with cooperatives. A key difference in this case is the close involvement of the value chain partners to ensure market access; a price incentive for improved practices and gear change; and technical support. Building-in a financial incentive for the cooperative and its members to change practices is a key consideration in the process, as is building a financial track record for the organization and its members to permit them to effectively access financing from the formal banking sector in the future.

A key finding of Csaky’s 2014 dissertation (4) was that “Cooperatives are at a disadvantage compared to other producer organization (PO) forms in achieving the conditions of global value chain access.” Additionally, lead firm driven efforts linking smallholders to markets like the international crab market have been more successful than those initiated by producers, i.e., top-down efforts are more successful than bottom-up efforts in these markets. In light of this, Wilderness Markets is actively exploring how the cooperative structure, which is recognized in Indonesia, can be formally partnered with existing value chain actors to effectively achieve financial, social and fishery management objectives to create a hybrid structure.

1. The terms “producer organization” and “cooperative” have different legal implications in different countries. Here we use producer organization in keeping with the original authors language or as an umbrella term that includes multiple forms of producer organizations, including cooperatives.

2. Dalberg. “Farmer Aggregation and Access to Finance”. 2013. Presentation. http://www.ico.org/documents/cy2012-13/forum/forum-3-zook-e.pdf

3. Csaky, Eva Szalkai. (2014). “Smallholder Global Value Chain Participation: The Role of Aggregation” (Unpublished doctoral dissertation). Duke University, Durham, NC. http://dukespace.lib.duke.edu/dspace/bitstream/handle/10161/9384/Csaky_duke_0066D_12557.pdf?sequence=1

4. Ibid

![Iceland - Siglufirði Siglufjörður By Hansueli Krapf This file was uploaded with Commonist. [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons](https://upload.wikimedia.org/wikipedia/commons/4/4b/2014-04-29_11-04-49_Iceland_-_Siglufir%C3%B0i_Siglufj%C3%B6r%C3%B0ur.JPG)

{kind=link}