Impact investors are ready to invest increasing amounts of impact capital in sustainable fisheries; what’s missing are profitable businesses and organizations with the capacity to accept investment. These profitable “investible entities” aren’t emerging apace because the entrepreneurial ecosystem to develop their business capacity is lagging.

Tag: constraints

-

How to Develop Impact Investment Opportunities in Sustainable Fisheries

The Need for Sustainable Fisheries Finance

We know all the problems associated with overfishing and we know that research shows:

1) that switching to more sustainable management will lead to increased revenues and food security; and

2) the cost for doing so exceeds what can be provided through traditional development and philanthropic organization.How do we get past the second to make the first possible? Supported by the World Bank, and with input from dozens of impact investors and fishery experts, we detail the main barriers and potential approaches to overcome them in our latest paper: Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries.

Who Should Read This Paper

This paper provides an overview for international development organizations, development finance institutions, NGOs, and the governments they work with of (i) the key concerns that impact investors may have when considering the financing of sustainable fisheries, and (ii) potential approaches for public-private partnerships to overcome these obstacles. It is intended as a primer for these actors, to understand the perspective of the commercial impact investor.

Overview

This paper explains the central challenges that keep impact investors from participating in sustainable fisheries, and is structured along four main barriers:

- A lack of reliable fishery data

- Ineffective fisheries management

- Unreliable infrastructure systems

- A paucity of investment-ready enterprises

It then proposes three models for sequencing and combining different sources of capital to overcome these obstacles:

- Serial approach: Public and philanthropic funders first support the establishment of strong governance arrangements, improved data collection, and fishery management. Once these initiatives mitigate some of the risk associated with a fishery investment, then return-seeking investors are incentivized to finance sustainable infrastructure projects (often through public-private partnerships) and/or enterprises along the value chain, focused on outcomes that achieve a triple bottom line: social responsibility, economic value, and environmental impact.

- Consolidated approach: Governments negotiate agreements with a single private sector entity or cooperative to delegate fishery management responsibilities. The private firm or cooperative then simultaneously invests in fishery data, management, infrastructure, and triple bottom line enterprises.

- Parallel approach: A range of investors and other stakeholders (for example, governments, nonprofit organizations, fishing collectives) develop coordinated investments to improve fisheries data, management, infrastructure, and triple bottom line enterprises. Efforts can be separately funded, but they work in tandem and share the ultimate goal of achieving sustainable catch with an appropriately capitalized and profitable fishing sector.

Each of these sequencing models presents particular challenges and opportunities. Structuring investments to achieve triple bottom line outcomes is still a new idea within the fisheries sector. There is growing evidence from other sectors, however, including agriculture and forestry, that these types of investments are achievable. Examples include the Moringa Fund[1] and Livelihood Funds,[2] which bring together public institutions, private investors, and NGOs, using innovative investment models to simultaneously address environmental degradation, climate change, and rural poverty while helping businesses become more sustainable.

The Impetus

Attracting impact investments is critical for the future of fishery recovery and expansion—these projects cannot rely on short-term loans and grants; they need longer-term finance that is committed to sustainability and responsibility. Development organizations, NGOs, and other noncommercial actors have a critical and catalytic role to play in crowding-in impact investment for sustainable fisheries by sharing risk with the private sector, promoting policy reforms, and funding interventions (through either concessional lending, grants, and/or technical assistance) with the intention of removing the barriers to impact investment.

Read the paper: Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries

[1] The Moringa Fund is a EUR 84 million investment fund that targets profitable large-scale agroforestry projects with high environmental and social impact in Latin America and Sub-Saharan Africa. The fund makes equity investments of EUR 4–10 million per project and adds value through its technical skills, environmental and social expertise, and global network.

[2] The Livelihood Funds are a series of investment funds created by Danone, which brings together investors—including Schneider Electric, Crédit Agricole S. A., Michelin, Hermès, SAP, CDC Climat, La Poste, Firmenich, and Voyageurs du Monde—to invest over EUR 40 million to finance nine on-the-ground programs for mangrove restoration, agroforestry, and rural energy.

-

Projected change in global fisheries revenues under climate change

A recent paper (September 2016) in the scientific journal of the National Institutes of Health exploring the implications of climate change on global fisheries revenues provides some sober reading.

The report explores how fisheries revenues of maritime countries will be impacted by climate change as a necessary “crucial next step towards the development of effective socio-economic policy and food sustainability strategies to mitigate and adapt to climate change”.

The report shows “that global fisheries revenues could drop by 35% more than the projected decrease in catches by the 2050 s under high CO2 emission scenarios. Regionally, the projected increases in fish catch in high latitudes may not translate into increases in revenues because of the increasing dominance of low value fish, and the decrease in catches by these countries’ vessels operating in more severely impacted distant waters. It finds that developing countries with high fisheries dependency are negatively impacted.”

See: Lam, Vicky W. Y. et al. “Projected Change in Global Fisheries Revenues under Climate Change.” Scientific Reports 6 (2016): 32607. PMC. Web. 18 July 2017.

The significantly higher impacts on developing country revenues both for export and domestic consumption are documented in the paper and provide further evidence to the risks climate change creates for wild capture fisheries.

-

Sustainable Fisheries – the role of the fishermen

Significant attention is being paid to the oceans. Between the UN Oceans Conference as the recent Economist leader, attention is (finally!) being given to the significant and numerous benefits and threats to the worlds oceans.

At a time of increasing populations, increased demand for healthy proteins – and arguably a climate imperative – human consumption of seafood is increasing exponentially. Wild capture seafoods are increasingly losing ground to aquaculture raised seafoods, for better or worse.

So why should we continue to care about wild capture seafoods? Isn’t sort of like expecting we should still live off wild buffalo and antelope?

It is – and the problem is, many emerging market countries are still dependent on wild capture fisheries for social, political and economic outcomes. Many emerging market economies depend on a sustained source of seafood to address social and poverty concerns. Fisheries related political decisions –in the form of subsidies and / or gear – are good politics at election time. And the national and global supply chains themselves are valuable sources of foreign currency in many countries.

While significant progress has been made to improve fisheries management in developed countries with strong rule of law, challenges remain on the open ocean and in many emerging markets. As summarized in a series of reports we completed, these challenges cut to the core of why fisheries remain “unmanaged”. We would argue that a developed world, legal first approach (which we call the “serial” approach) will not work in many emerging markets.

What is instead needed is a concerted effort to engage fishermen, gather reliable data and find culturally appropriate solutions in conjunction with the supply chain. These efforts can be complimentary – and inform – efforts to address legal and regulatory requirements in “parallel”, allowing fishermen to realize the benefits of changes in practices, presenting value chain actors and regulators with clear data on landings, and doing so in a culturally appropriate manner.

Our recent efforts in the United States and in Asia continue to support this theory.

In the United States, now that the west coast groundfish fishery is in recovery, fishermen face the reality that the market price is below the cost of landing the fish as management costs have increased while revenues have remained flat (or declined when adjusted for inflation) for the higher volume species. The market, in effect, compares US groundfish to imported white fish and sets the price at the lower of the two, in large part due to the volumes, but also due to the lower costs of imports. Unless prices and market access improve for US groundfish fishermen, its unlikely many of them will remain in business (and this in turn will imperil the funding of the fisheries management system).

In Indonesia, the bigger challenge relates to the lack of registration of fishermen and vessels, poor landings data and limited data on fishing sites and practices, particularly in artisanal fisheries which are increasingly being drawn into national and global supply chains due to the increased demand. In many countries, fishermen are essentially unregistered, have limited access to services and are not legally recognized. In nearly all the emerging market value chains we reviewed, the first legally recognized stage of the value chain was the aggregator or middle person. This legal recognition is important – it enables access to government and private services and it allows managers to define and engage with users.

It will continue to be challenging to manage these historically productive fisheries unless these challenges are addressed in a culturally appropriate manner.

Wilderness Markets is developing a range of measures building on the interests of fishermen that address these challenges in US and developing country fisheries. These include improving market access and recognition for fishermen with industry; addressing fishermen registration and organization; ensuring good data is collected and made available to all relevant parties as well as aligning economic incentives. An essential underpinning of all this work is the need to engage with, and facilitate, changes in practices in existing firms.

As we are seeing in our work, systems change is possible, it takes the combination of a bottom up approach and a systematic assessment of metrics to keep everyone on track.

-

West Coast Groundfish Pilot: What’s Next for Developing Local Markets?

A previous post outlined the results of the recent market demand research for West Coast groundfish. This post follows-up with more detail on the proposed West Coast groundfish pilot.

Purpose and Intent

And now what? That was our first question after learning the results from the market demand research. Those results indicated that next efforts to improve demand and pricing for West Coast groundfish should focus on selling minimally processed products to suppliers and buyers in the grocery retail and full service restaurant sectors. The answer is a pilot project; one designed to test the findings which will help U.S. West Coast fishermen expand into regional market.

This project would aim to raise commercial buyers’ and suppliers’ awareness of U.S. West Coast Groundfish as a domestic, sustainable source of whitefish and prove that these fisheries can provide a reliable supply of local fish. As a result, it will establish new markets and demonstrate the benefits and availability of West Coast groundfish to other buyers and suppliers.

Rationale

A pilot project, with defined sales periods and goals, will provide room to experiment to build relationships and to understand the market dynamics. Without a pilot, it will be difficult, if not impossible, to rally collaborative action or justify further investments in the fishery. Harvesters and buyers envision a pilot as being a first step in creating an ongoing sales effort that expands beyond the West Coast within two to three years, possibly sooner.

A successful pilot is key to having larger, sophisticated customers purchase significant quantities for a substantial part of their operations; the pilot also develops the tools they need to successfully use and continue purchasing the fish. Assuming the pilot results in positive values, harvesters, trusts, buyers, NGO’s, and potential investors will have information necessary to make decisions about infrastructure, marketing and other investments. In addition, they can start sizing-up plans in the local, regional and national markets, all of which are important to increasing quota attainment.

Framework

To create organizational capacity that endures beyond the period of the pilot, it needs to be structured carefully. The fishermen and the buyers need to feel comfortable with their roles and build knowledge useful for future efforts. Because of this, the pilot project will endeavor to work within the existing supply chain to build the ability of the harvest groups and processors to provide reliable supply. Memorandums of understanding and contracts for the pilot have to be written so all the parties involved understand their roles and feel comfortable with their responsibilities. Of utmost importance, the pilot design must incorporate a way for the value chain to continue the work after the pilot concludes.

Target Outcomes

Some specific questions the pilot should be designed to answer revolve around the conditions and requirements for supply and pricing. At the outset, stakeholders will need to address legal restrictions on collaboration. The pilot should also define the incentives or conditions needed to gain cooperation between the processors and the groundfish harvesters. Also, the pilot should delineate the amount of fish, prices, and timing (flow of supply and seasons). Finally, the pilot will try to determine the level of transparency needed to build trust so that value chain actors can work together as a team to create value.

Final Thoughts

Regardless of who carries out the work, a pilot is the best next step for the West Coast groundfish stakeholders. The ultimate goals are easy – improve profits for those paying for management – but the route has to be carefully plotted. Building trust and knowledge and demonstrating improved values are key. We can get there, but we have to keep the focus on the end goal of a sustainable fishery, which means ensuring profitability for the harvesters.

-

Lead Firm Strategy Implementation – Indonesian Blue Swimming Crab

Overview

In 2015, Wilderness Markets completed a value chain summary of the blue swimming crab (BSC) fishery in Indonesia in which we analyzed the current state of fishery data systems, resource management, infrastructure, and enterprise capacity. Based on these findings, we recommend a lead firm strategy to move the fishery toward sustainability. Like many fisheries in emerging markets, the Indonesian BSC fishery lacks reliable data and, despite new national policies, functions largely without effective management. The value chain has strong, established commercial and social relationships, indicative of the power and influence of a small group of 16 processors buying from 400 mini-plants that, in turn, purchase crab from more than 65,000 fishermen.

In this case, the lead firm is a U.S. based company, Blue Star Foods. Blue Star is working to create financial and social incentives to enable fishermen to transition faster to sustainable fishing practices. Through its purchasing power and relationships, Blue Star is therefore in strong position to influence the practices of a range of processors, who have commercial relationships with a network of mini-plants, collectors, and fishermen.

Sumatran vessel with collapsible traps Lead Firm Pilot Design

With Blue Star and local harvesters, we are developing an investment model based on a pilot partnership between the lead firm and a fishing cooperative (in development). The model brings together philanthropic and private capital and provides financial, social, and environmental returns. It includes:

- Purchase commitments based on price, quality and standards

- Investments in fishermen cooperatives to motivate gear improvements

- Improved fishery data collection and traceability

- Support for harvest control compliance

This pilot is designed to attract private, return-seeking impact investment and complement ongoing work by NGOs to improve fishery management. We expect this approach will enable local fishermen to adopt sustainable practices faster than waiting for the government to independently create and enforce management changes, and without the economic hardship for fishermen that often accompanies changes in fishery regulations. It will also bolster business advocacy for more effective fisheries management policies and enforcement through a local cooperative structure.

BSC fisherman with new vessel tracking device Goals and expected outcomes

Ultimately, as a result of better data collection and effective management, the fishery will produce higher yields of BSC. It will also provide a traceable, sustainably harvested product with a competitive advantage in key U.S. and E.U. markets. This will then allow Blue Star and supporting investors to recoup their investments in sustainable practices.

By embedding this lead firm work within existing value chain relationships and practices, we aim to:

- Demonstrate the financial viability of investments in fishery data collection and management, thus attracting additional private investment in these practices.

- Create new norms that are sustained because of their business value and not ongoing philanthropic support or government subsidies.

- Provide clear and reliable financial benefits for small-scale fishermen to make gear changes; follow harvest control measures; and take on other sustainable fishing practices. Immediate economic well-being is thereby aligned with sustainable practices to improve compliance and reduce the localized short-term, negative impacts of fishery restrictions.

- Finally, test a new, “parallel” investment model for combining philanthropic, government, and private sector funding to address fishery management. If successful, other emerging market fisheries can tailor the model.

We are currently seeking additional partners to join us in this lead firm pilot project. Please get in touch with us if you would like more information and/or would like to get involved.

-

What does stock health tell us about potential investments?

What’s an easy way for an investor to tell if a natural resource-based enterprise is going to be viable in three to five years? Part of that answer lies in evaluating the business and the regulatory environments in which it operates, but for natural resources in particular, the resource base trend needs to be examined; is it predicted that there will be more or less in the future, based on current extraction rates and scientific estimates of the resource level? And for conservation-focused impact investments, how can investors ensure they are not using more than the ecosystem can sustain?

In wild-capture fisheries, this translates to: “Will there be more or less of the fish to harvest in the future? Will my investment exacerbate overfishing?” Less fish to harvest means the effort level, and thus costs, will need to increase to find the remaining fish.

We’ve recently been puzzling through the easiest way for banks and impact investors to gauge the investability of fisheries enterprises, with a focus on Indonesia. Indonesia hosts some of the most biodiverse ocean ecosystems on our planet and is the world’s second largest harvester of wild capture fish. Banks and investors need quick, easily understood data that doesn’t unnecessarily burden their due diligence process but ensures they aren’t contributing to overfishing.

One tool that is already available in many fisheries is the stock assessment status, usually indicated as under- or moderately exploited, fully exploited, or over-exploited. The exploitation levels reflect scientific data on whether the fish in a fishery (the stock) are being sustainably harvested. Fully exploited indicates a stock that is thought to be fished and reproducing at nearly equal rates, i.e., the amount of fish harvested is the same as the fish being hatched and surviving to maturity. Over-exploited means harvest rates are too high, and under-exploited means they could increase rates without having a harmful effect on stocks.

Indonesia’s Ministry of Marine Affairs and Fisheries recently released the results of the National Commission on Stock Assessments (NOMOR 47/KEPMEN-KP/2016 TENTANG). The assessment provides an updated snapshot of ministry data in each fishery management area for the status of nine Indonesian fishery stocks.

In addition to focusing government investments on improving the fishery health, we think the data can be useful for banks and investors. The assessment data can help investors quickly determine the potential health of the resource an enterprise relies on, helping to ensure they are not causing more fish to be used than can be replaced. The key to balancing conservation and investment entails finding new opportunities to do more, without using more.

Disclaimer

The findings and conclusions in this report represent the interpretations of Wilderness Markets and do not necessarily reflect the view of expert stakeholders. This publication has been prepared solely for informational purposes, and has been prepared in good faith on the basis of information available at the date of publication without any independent verification. Wilderness Markets does not guarantee or warrant the accuracy, reliability, adequacy, completeness or currency of the information in this publication nor its usefulness in achieving any purpose. Charts and graphs provided herein are for illustrative purposes only. Nothing contained herein constitutes investment, legal, tax, or other advice nor is it to be relied on in making an investment or other decision. Readers are responsible for assessing the relevance and accuracy of the content of this publication. this publication should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell securities or to adopt any investment strategy.

-

What lessons can be learned from the Icelandic cod value chain?

![Iceland - Siglufirði Siglufjörður By Hansueli Krapf This file was uploaded with Commonist. [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons](https://upload.wikimedia.org/wikipedia/commons/4/4b/2014-04-29_11-04-49_Iceland_-_Siglufir%C3%B0i_Siglufj%C3%B6r%C3%B0ur.JPG)

Iceland – Siglufirði Siglufjörður By Hansueli Krapf This file was uploaded with Commonist. [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons

Icelandic cod first came to our attention at Wilderness Markets when we were collaborating with Future of Fish on research into financing needs in the US Northeast Multispecies Sector Program. How can cod from, Iceland, over 2000 miles away be not only cheaper but of equal or better quality than cod caught from just outside your proverbial front door?

A series of papers highlights important developments and key factors in the success of the Icelandic cod value chain since the ‘90s. The series include:

- The Effects of Fisheries Management on the Icelandic Demersal Fish Value Chain, 2016[1]

- A Comparison of the Icelandic Cod Value Chain and the Yellow Fin Tuna Value Chain of Sri Lanka, 2010[2]

- The Role of Fish Markets in the Icelandic Value Chain of Cod, 2010[3]

- The Importance of SMEs in the Icelandic Fisheries Global Value Chain, July 2009[4]

- Structural Changes in the Icelandic Fisheries Sector – A Value Chain Analysis, 2008[5]

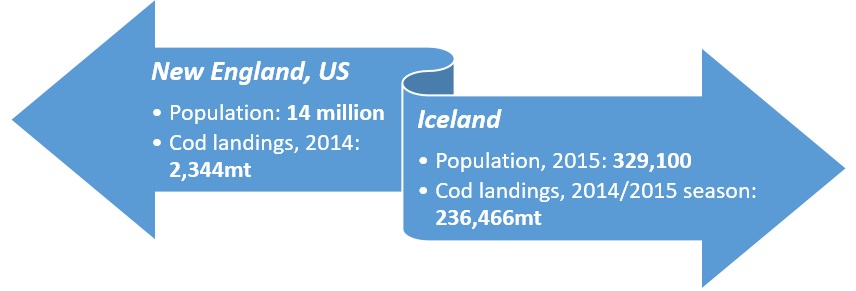

Before digging in too far, two aspects of the Icelandic versus the New England value chains can’t be overlooked—the relatively small population of Iceland and the relatively high landings of cod. For disputed reasons (climate change, better management, etc.) Iceland has a much healthier, i.e. more abundant stock, and hundred-fold greater landings than New England. Along with much higher landings, a far lower population means a robust export market.

Key factors and developments:

- Increased efficiency at multiple levels of the value chain has helped improve value

- Domestic value creation, specifically in the form of fresh fillets, has added significant value

- Information flow (availability of information) and knowledge drive value

- Use of marketing information to govern the value chain through vertical integrated companies and fish auction markets

- Fish markets (auctions) improve efficiency and improve the consistency of supply for the value chain by acting as clearinghouses and support speculation

- Consolidation of vessels, fishermen, processors, processing workers, and quota ownership have occurred in significant number

- Increased specializations in fishing and processing

An interesting aspect that warranted a whole paper is the role of the fish markets, effectively online auctions, wherein all bidding is done through one computerized system owned by 15 independent markets since 2000. These private markets only handle 20% of the landings by volume but have a high value in terms of value chain efficiency because they allow for specialization (buyers can sell or swap species not needed for production), provide stability (buyers can ‘top-up’ if they are short on supply) and creates market-driven value for species. The rise in general groundfish prices by 20% from 1999 to 2008 is thought to be partially attributed to the fish market system.

Some key aspects of the Icelandic cod value chain, like low human population in Iceland and abundance of target species in their waters, don’t readily translate to Wilderness Markets’ recent focus on the Indonesian and U.S. West Coast fisheries. Others do. For instance, in the paper on the importance of small and medium enterprises (SMEs), the increase in vertically integrated companies means those companies have better control of the reliability, quality and delivery of fisheries products. Their competitive advantages are related to quality assurance knowledge, good logistics and dedicated export and sales management. On an almost reverse timeline for the U.S. West Coast groundfish fishery in California, fish handling in Iceland improved in the ‘90s and ‘00s by investments in better onboard cooling systems, shorter fishing trips and logistics improvements.

In the 2016 paper, they also describe the structure of the value chain before the export licensing system was abolished in the 1980s—importantly, and with implications for other value chains – the three large marketing and sales organizations that controlled most of the fish failed to send market signals back to producers. The new, vertically integrated companies that replaced these organizations heeded signals from foreign customers and improved product quality and successfully added value domestically by switching processing to Iceland instead of overseas.

We have witnessed this same disconnect in many other fisheries; fishermen don’t seem to have any idea about the needs and demands of the end markets and have no incentive to meet these demands. In one of the most telling statements in the series, an interviewee states, “They [the Norwegians] are still mostly thinking about catching while we have reached the point where we think about serving the market.” Most fishermen have not yet been able to reach this stage, hindering their ability to realize improved value for their work.

We’re hopeful that the end-market research currently underway in California will provide market data that can be turned into increased value for the harvesters working diligently to promote sustainability.

[1] Knútsson, Ö., Kristófersson, D. M., & Gestsson, H. (2016). The effects of fisheries management on the Icelandic demersal fish value chain. Marine Policy, 63, 172-179..

[2] Knútsson, Ö., Gestsson, H., Klemensson, O., Thordarson, G., & Amaralal, L. (2010). A Comparison of the Icelandic Cod Value Chain and the Yellow Fin Tuna Value Chain in Sri Lanka.

[3] Knútsson, Ö., Klemensson, Ó., & Gestsson, H. (2010). The Role of Fish-Markets in the Icelandic Value Chain of Cod.

[4] Knútsson, Ö., Gestsson, H., & Klemensson, Ó. (2009, July). The importance of SMEs in the Icelandic fisheries global value chain. In IXX EAFE Conference Proceedings (pp. 6-9).

[5] Knútsson, Ö., Klemensson, Ó., & Gestsson, H. (2008). Structural changes in the Icelandic fisheries sector-a value chain analysis.

[6] New England Population: http://www.dlt.ri.gov/lmi/census/pop/neweng.htm

Iceland Population: http://www.iceland.is/the-big-picture/quick-factsUS landings: http://www.st.nmfs.noaa.gov/commercial-fisheries/commercial-landings/annual-landings/index

Icelandic landings: http://icefishnews.com/wp-content/uploads/2013/05/Marko-partners-%C3%ADslenski-kv%C3%B3tinn.png -

Sustainable Fisheries Investments: Lessons from the Field

Three years ago, we set out to to explore a perceived anomaly in the impact investment market. While sectors such as carbon and agriculture were attracting a range of capital investment in sustainable fisheries appeared to be neglected. Given the geographic scope, industry scale and potential impact, we wanted to understand the reasons behind the lack of capital.

Our conclusion, following three years of field based research and due diligence in three countries, five fisheries, and over 220 interviews with financial, corporate, government, community and NGO representatives, identified the following key constraints:

- Data

- Management

- Market differentiation

- Infrastructure

- Finance

- Lack of investable entities

The first two, data and management, are the most pressing constraints to the effective deployment of capital at scale in developing country fisheries (DCFs), as discussed in our recently released report, “Connecting the Dots”. Each need to be addressed simultaneously if equitable participation of the harvester is important to investors.

Concerning specific investments, there’s a fundamental need to distinguish between who and what benefits from value chain investments and investments in the drivers of stock health. While a healthy value chain benefits from a healthy stock, the benefits do not cut both ways, that is, a healthy value chain does not necessarily make stocks healthier; the drivers of stock health must be addressed.

Another general assumption holds that by changing the practices of one or two players in the value chain, we can secure stock health – this was found to be exceedingly unlikely in the open access system of fisheries which suffer from the tragedy of the commons. Addressing artisanal tuna harvester needs is socially and potentially economically positive, but it is difficult to prove environmental benefits if the next village over has unrestricted access – along with the purse seine factory fishing boat from the country next door!

The drivers of stock health are all external to the value chain, and, unfortunately, most financial interventions are reliant on the value chain in order to secure repayment. This disconnect is seldom recognized by practitioners, and it is often assumed that by changing the practices of one or two players in the value chain, we can secure stock health. At the other end of the spectrum are improvements aimed at stock health and improved socio-economics for fishing communities that rely on the “build it and they will come” theory, failing to integrate harvesters and buyers into improvements.

Our findings are that value chain based investments in open access systems are unlikely to improve environmental outcomes, and, in practices, are likely to accelerate resource extraction, in some cases, of already pressured stocks and resources.

Our research also identified significant investments in fisheries are an ongoing reality in many DCFs. Whether from the private sector (DDI and DFI data), and from national governments, fisheries are well capitalized.

The inequality experienced by artisanal harvesters is not, in our view, an issue of capital. It is a systemic failure, requiring multiple components be addressed simultaneously

There is an urgent need to focus efforts on improving the drivers of stock health in DCFs, over and above deploying yet more capital into the value chain without investment in stock health.

-

Markets for Groundfish in California, Part 1 of 4

This is part 1 of a 4-part series intended to invite conversations in advance of our planned end market demand analysis for groundfish in California. The larger goal is to provide quantified end market data to inform profitable value chain investments that will positively impact harvesters, local communities and the ocean. (more…)

{kind=link}