Impact investors are ready to invest increasing amounts of impact capital in sustainable fisheries; what’s missing are profitable businesses and organizations with the capacity to accept investment. These profitable “investible entities” aren’t emerging apace because the entrepreneurial ecosystem to develop their business capacity is lagging.

Tag: change

-

Marine Heat Waves More Common and Lasting Longer Globally

A study done by the Marine Heatwaves International Working Group showed that there has been a 54% increase globally in the number of “marine heat wave days” per year since 1925.[1] Published in the Nature Communications journal and cited in News Deeply recently[2], the study cited the warm zone off the Western Australian coast in 2011 and the Gulf of Maine episode in 2012 as incidences of this trend. Average ocean temperatures have been increasing but these marine heat waves are also increasing in frequency and duration. The combination of the two are linked to factors that damage ecosystems and economies.

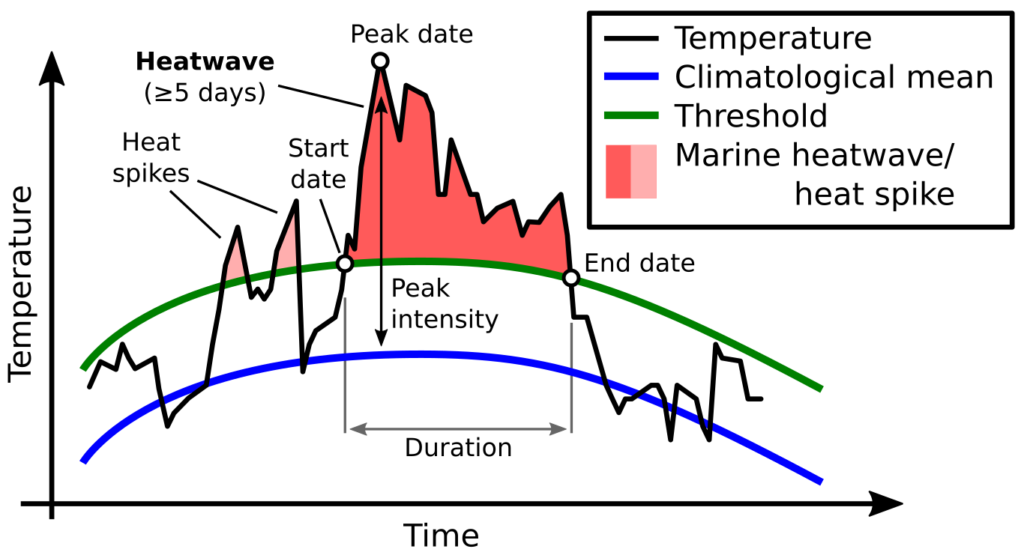

Figure 1 Graphic explanation of Marine Heat Waves, from http://www.marineheatwaves.org/all-about-mhws.html

Marine heat waves (MHWs) are “…prolonged periods of anomalously high sea surface temperatures… [that] have had severe impacts on marine ecosystems in recent years.” (Oliver et al., 2018). In Australia alone, Shark Bay in Western Australia lost 36% of its seagrass meadows and carbon storage, and the Great Barrier Reef suffered four mass coral bleaching events because of these extended periods of elevated sea surface temperatures.[3]

There are significant ecological and economic effects arising from these marine heat waves. They include:

“… sustained loss of kelp forests, coral bleaching, reduced surface chlorophyll levels due to increased surface layer stratification, mass mortality of marine invertebrates due to heat stress, rapid long-distance species’ range shifts and associated reshaping of community structure, fishery closures or quota changes and even intensified economic tensions between nations.” (Oliver et al., 2018)[4]

According to Eric Oliver, the study’s lead author, “…in the early 20th century, there was an average of two marine heat waves per year globally, but now there are three or four. While they used to last 10 days on average, they now last for an average of 13 or 14 days.”[5]

The study suggests that marine heat waves will continue to increase with the ongoing global warming.

Why does Wilderness Markets care about anemones and anemonefish? Because our work requires us to look not only at enterprises and fishery management, but at the entire ecosystem to properly account for business risks. Learn more about us.

[1] Oliver, E. C. J et al. (2018). Longer and more frequent marine heatwaves over the past century. Nature Communications, 9. doi: 10.1038/s41467-018-03732-9

[2] News Deeply. (2018). Executive Summary for April 13th. Oceans Deeply (Marine Heatwaves Are Longer, More Frequent). Retrieved from https://www.newsdeeply.com/oceans/executive-summaries/2018/04/13.

[3] McSweeney, R. (2018). Marine heatwaves have become ‘34% more likely’ over past century. Carbon Brief. Marine heatwaves have become ‘34% more likely’ over past century. Retrieved from https://www.carbonbrief.org/marine-heatwaves-have-become-34-more-likely-over-past-century.

[4] Oliver, E. C. J et al.

[5] Willick, F. (2018). Ocean heat waves becoming more common, longer, new study finds. CBC. Retrieved from http://www.cbc.ca/news/canada/nova-scotia/marine-heat-wave-ocean-hot-spot-study-1.4611794

-

Climate Change Stresses Clownfish

Rising ocean temperatures are causing significant changes with devastating impact on the ecosystem. Worldwide, the warmer and more acidic ocean conditions in the tropics have caused mass bleaching of anemones and corals[1]. A new study published in the Proceedings of the Royal Society B supports findings from another recent study in the journal, Nature, that the bleaching of anemones has a severe impact on anemonefish, like clownfish and dire consequences for marine life in general.[2]

Clownfish in anemone. Used under Creative Commons from : https://pxhere.com/en/photo/559857 Findings

The latest study looked at the metabolic rates between fish from bleached and unbleached anemones. Even though there was no discernible difference in activity between the two groups of fish, the study found that the “[s]tandard metabolic rate of anemonefish from bleached anemones was significantly higher by 8.2% compared with that of fish residing in unbleached anemones, possibly due to increased stress levels.”[3] Reduced spawning frequency and lower fecundity are two of the negative impacts that were previously observed.

The study published in Nature in 2017 focused on the hormonal stress response and reproduction of anemonefish in bleached anemones. The 14-month monitoring study found a strong correlation between the anemone bleaching and the anemonefish’s stress response and reproductive hormones. Anemonefish in bleached anemones had a 73% decrease in fecundity compared to anemonefish in unbleached anemones. They spawned half as frequently, laid 64% fewer eggs, and experienced a significantly higher egg mortality in incubation. The authors were unable to determine why the bleaching of anemones would trigger a stress response in anemonefish. They offer the possibility that bleached anemones may provide less cover and have reduced neurotoxicity of venom which leads anemonefish to perceive a greater risk of predation. [4]

According to Beldade, Agathe, O’Donnell, & Mills (2017), there are “…[a]t least 50 species of fishes and facultative symbionts of sea anemones worldwide…as many as 12% (56/464) of coastal fish species depend directly, either for food or shelter, on organisms capable of bleaching. While the strength of such dependency varies greatly, if these species suffer even a fraction of the impact found for anemonefish, then a short-lived bleaching event could decrease the reproductive output of at least 12% of species, especially those highly dependent on corals or anemones.”

Takeaway

The two studies contribute to a growing library of research on the effects of global warming on marine life and highlights the importance of understanding how individual differences in stress responses influence a species’ chances of survival.

Why does Wilderness Markets care about anemones and anemonefish? Because our work requires us to look not only at enterprises and fishery management, but at the entire ecosystem to properly account for business risks. Learn more about us.

Photo Credit: “q phia”; anemone fish on bleached anemone, fukui, siladen, 2017 [1] Norin, T, Mills, S. C., Crespel, A., Cortese, D., Killen, S. S., & Beldade, R. (2018). Anemone bleaching increases the metabolic demands of symbiont anemonefish [Abstract]. Proceedings of The Royal Society B. doi: 10.1098/rspb.2018.0282

[2] News Deeply. (2018). Executive Summary for April 13th. Oceans Deeply (Bleaching of Anemones Makes Life Harder for Clown Fish). Retrieved from https://www.newsdeeply.com/oceans/executive-summaries/2018/04/13.

[3] Norin, et al.

[4] Beldade, R., Blandin, A., O’Donnell, R., & Mills, S. C. (2017). Cascading effects of thermally-induced anemone bleaching on associated anemonefish hormonal stress response and reproduction. Nature Communications, 8. doi: 10.1038/s41467-017-00565-w

-

Improve Data to Improve Sustainability

Case Study:

Developing and Implementing SIMP Compatible Seafood Data Reporting and Traceability System in the Crab Supply ChainProblem Statement and Opportunity

The U.S. implementation of the Seafood Import and Monitoring Program (SIMP)[1] on 1 January 2018 establishes reporting and recordkeeping requirements to prevent illegal, unreported and unregulated (IUU) seafood from entering the U.S. The onus of proof is placed on the importer of record to provide and report key data from harvest to U.S. entry. In geographically diffuse supply chains, like blue swimming crab from Southeast Asia, with thousands of “points of entry”, i.e., fishers, tracking landings to the vessel is far less straightforward than short and narrow supply chains, such as skipjack tuna or sardines. This reporting requirement, while worthwhile, will require U.S. seafood importers to incorporate cost-effective traceability initiatives in their often-complex supply chains.

There is a growing appreciation that the needs of fishers and their communities must be addressed in order to improve the underlying causes of fishery exploitation in the developing world, particularly for small-scale fisheries. -California Environmental Associates

The requirement also presents an opportunity to promote resource sustainability through supply chain transparency and catch monitoring. Despite pledges to abide by size limits, U.S. importers of blue swimming crab (BSC) have difficulty ensuring their supply chain partners are buying only crabs larger than the agreed minimum size of 10cm and excluding berried females. The application along with a web-based reporting tool we developed can meet the requirements of the SIMP, as well as the European Catch Documentation (CD) requirements, and elucidate the in-country supply chain. By tracking landings by vessel and by harvester, this tool further provides the opportunity to address key social and environmental outcomes associated with the Sustainable Development Goals[2] (SDGs), which gives seafood importers a mulit-purpose toolkit to both decrease their reporting costs and increase the sustainability of the crab stocks.

The opportunity to spur social and economic impact should not be underestimated. Educating, engaging and rewarding fishers and communities directly for complying with ecological goals like minimum size, berried females, no-take areas, and more offers an opportunity to engage communities directly in resource management and provide key links to SDGs. Aside from nascent work by Fair Trade[3] and SmartFish[4], there are few fishery sustainability efforts that actually benefit the fishers that form the foundation of many supply seafood chains. Indeed, most efforts impose costs on fishing communities—time, foregone income, capital for new equipment—without providing benefits. Our tool allows identification of compliant fishers, so they can be awarded price premiums and other incentives.

Supply chain transparency is beneficial to the U.S. importer not only in terms of identifying good actors and meeting reporting requirements, but also gives them an edge in the marketplace full of otherwise opaque supply chains.

Provision of ice is a key concern Assessment

When initially considering how to provide BSC supply chain transparency from the ocean to the end buyer, we researched existing options, hoping to find one that could be customized to the supply chain. We conducted a desk review, scouring the internet and our personal network to identify all available options. In total, we reviewed nearly forty systems that provided varying levels of traceability; of these, we interviewed approximately six potential providers that met or came close to our key considerations:

- Ease of use – the user interface needed to be easy for data collectors in Indonesia and importers in the U.S. to use

- Utility for marketing purposes – a consumer-facing component was a must

- Facilitate regulatory compliance – must collect and provide data required by the SIMP and EU CD in a straightforward format

- Mapping – needs to provide maps of fishing locations to determine which areas are best for avoiding undersized and berried crabs

- Business model – a cost effective and durable business model that did not result in excessive fees or costs to each level of the value chain

- Data access, storage and ownership – data must be accessible by multiple parties within the value chain, stored in Indonesia, and owned by the funding company

- Reasonable set-up costs – ideally, a system would be compatible with existing software and hardware and would require little in the way of training. A team should be able to begin data collection with a few hours or less of upfront training on the system interface and they should be able to readily convey to the fishers the benefits of the system.

- Geographic and cultural relevance – the system needed to function in rural, relatively isolated areas with little to no telecommunications access

- Engage Harvesters and Vessel owners in order to build their understanding and the relative importance of adhering to harvest control regulation

- Ease of integration – overall, the platform needed to be easy to readily integrate into the supply chain.

Findings from Assessment

None of the reviewed systems met the requirements of the lead firm with the exception of the Pelagic Data Systems units for vessel management, i.e., vessel tracking. Due to the cost of acquisition and the relatively high ongoing costs of use, these were installed on a trial basis. This test was not successful, and cheaper, more effective units were identified.

Development

Not finding a suitable existing program, Blue Star Foods decided to develop their own application to gather data tied to their marketing goals and objectives around supply chain integrity. The SIMP and EU CD data requirements were integrated into the data collection system. Wilderness Markets worked closely with an app-development team to develop an Android and iOS application and support the field trials. After the initial field trials, the system was deployed to in-house teams from Blue Star Foods Indonesian partners, consisting of procurement and quality control specialists.

Implementation and Deployment

Data was collected at selected mini-plants and landing sites during a six-month period. Both harvesters and data collectors were simply encouraged to log landings during the pilot phase without any indication or reference to IUU or other considerations. They were not penalized or otherwise reprimanded for reporting undersized or berried crabs during this time period. Vessel tracking data was collected for a select number of boats during this period, which could be matched to landings data.

Sumatran Fisherman with Blue Swimming Crabs Initial learning points

- Data collection required additional training of procurement and quality control teams. This in turn required an additional budget to be implemented effectively.

- The pilot only covered a small portion of overall U.S. imports from Indonesia (less than 1%) – the current opacity of the supply chain means we did not know how much each mini-plant contributes to the supply chain before the pilot

- The system efficiency is high enough that recording all landings at a mini-plant or at a landing site is possible, though unless a quality control individual is onsite continually, it cannot guarantee there will be no side selling unless all buyers agree to use the system.

- The data feedback loop to management has been significantly shortened and is possible in nearly real-time allowing:

- Faster identification of low productivity landing sites

- Faster identification of high productivity landing sites

- Faster identification of undersized and/or berried crab seasons and locations

- Data integrity and accuracy continues to be an issue and needs to be worked on – Due to their small size, most vessels are unregistered so vessel identification is challenging. Usual data integrity and accuracy issues for data collection operations exist, such as ensuring consistent data entry, checking entries for errors, etc.

Initial Data Findings

- Initial indications, based on sampling approximately 10% of the harvest per vessel, are that up to 25% of landings can likely be classified as IUU (berried females & sub 10cm).

- Boats with lowest supply chain loyalty appear to have higher levels of IUU (an assumption to be tested in additional sites)

- It is now possible to identify the specific boats that are causing the high levels of infractions, and to address with through the supply chain in a focused manner.

- Less than 20% of the surveyed vessels were responsible for 80% of the IUU landings

Fishery Management Implications

The ability to specifically identify vessels not complying with agreed harvest controls will permit a more targeted, focused and cost-effective approach to monitoring and enforcement of infractions. With less than 20% of the vessels are causing 80% of the issues with regards to IUU landings, efforts can be made to reduce IUU in a focused manner.

The data provides:

- Ability to provide shore-based landing information

- Ability to identify both geographic and seasonal potential closure options based on real data

- Ability to target enforcement based on recorded infractions

BSC fisherman with new vessel tracking device Links to SDGs

In addition to the business and fishery management implications, the findings are directly linked to at least three SDGs:

SDG 8 Decent Work and Economic Growth

Promote sustained, inclusive and sustainable economic growth, full and productive employment and decent work for all

Biological data indicates a quick (less than 1 year) stock recovery when undersized crabs are left in the water, thereby increasing the economic value of the fishery and decoupling growth from environmental degradation (Target 8.4)

SDG 9 Industry, Innovation and Infrastructure

Build resilient infrastructure, promote inclusive and sustainable industrialization and foster innovation

Increasing the transparency of the supply chain means that small-scale enterprises, like the mini-plants, can have better access to financial services (Target 9.3).

SDG 14 Life Below Water

Conserve and sustainably use the oceans, seas and marine resources for sustainable development

Using the data generated by the app, progress can be made towards sustainably managing fish stocks, combatting IUU, and providing meaningful market access for small-scale artisanal fishers (Targets 14.4, 14.6 and 14.B).

Recommendations and Next Steps

A key recommendation of the initial pilot is the need to establish unique vessel IDs with the support of local government authorities, which will allow more meaningful monitoring and enforcement of landings.

In addition, the need to engage with, and involve, other firms purchasing from the fishery was identified in order to reduce the opportunities for side selling.

A second phase is being planned to address the constraints of the first. The goal of the second phase is to:

- Capture a minimum of 25% of the Blue Star Foods Indonesia sourcing;

- Integrate improved vessel activity geographic data

- Expand geographically

- Include more processors, mini-plants and fishers in Indonesia, particularly in co-packer conditions

- Replicate into the Blue Star Foods Philippine supply chain

Conclusion

The drivers of market access compliance requirements, improved social and financial impact in in artisinal fisheries and greater supply chain integration are powerful drivers for change in any industry. The relatively low cost now associated with data capture tools mean lead firms can utilize almost ubiquitous cell phone availability to cost effectively assess the degree and extent of IUU in their supply chain, while strengthening their impact objectives and improving market recognition.

This approach provides resource managers and NGOs as well as development agencies with a relevant, cost effective tool to engage private sector supply chains in achieving SDGs in a measurable, informed and data driven manner.

[1] “U.S. Seafood Import Monitoring Program”. Retrieved on 7 March 2018 from: https://www.iuufishing.noaa.gov/RecommendationsandActions/RECOMMENDATION1415/FinalRuleTraceability.aspx

[2] “Sustainable Development Goals”. Retrieved on 19 March 2018 from https://sustainabledevelopment.un.org/?menu=1300

[3] “Capture Fisheries Standard (CFS)”. Retrieved on 8 March 2018 from: https://www.fairtradecertified.org/business/producer-certification

[4] “Rescate de Valor”. (English: Value Rescue) Retrieved on 8 March 2018 from: http://rescatedevalor.org/

-

How to Develop Impact Investment Opportunities in Sustainable Fisheries

The Need for Sustainable Fisheries Finance

We know all the problems associated with overfishing and we know that research shows:

1) that switching to more sustainable management will lead to increased revenues and food security; and

2) the cost for doing so exceeds what can be provided through traditional development and philanthropic organization.How do we get past the second to make the first possible? Supported by the World Bank, and with input from dozens of impact investors and fishery experts, we detail the main barriers and potential approaches to overcome them in our latest paper: Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries.

Who Should Read This Paper

This paper provides an overview for international development organizations, development finance institutions, NGOs, and the governments they work with of (i) the key concerns that impact investors may have when considering the financing of sustainable fisheries, and (ii) potential approaches for public-private partnerships to overcome these obstacles. It is intended as a primer for these actors, to understand the perspective of the commercial impact investor.

Overview

This paper explains the central challenges that keep impact investors from participating in sustainable fisheries, and is structured along four main barriers:

- A lack of reliable fishery data

- Ineffective fisheries management

- Unreliable infrastructure systems

- A paucity of investment-ready enterprises

It then proposes three models for sequencing and combining different sources of capital to overcome these obstacles:

- Serial approach: Public and philanthropic funders first support the establishment of strong governance arrangements, improved data collection, and fishery management. Once these initiatives mitigate some of the risk associated with a fishery investment, then return-seeking investors are incentivized to finance sustainable infrastructure projects (often through public-private partnerships) and/or enterprises along the value chain, focused on outcomes that achieve a triple bottom line: social responsibility, economic value, and environmental impact.

- Consolidated approach: Governments negotiate agreements with a single private sector entity or cooperative to delegate fishery management responsibilities. The private firm or cooperative then simultaneously invests in fishery data, management, infrastructure, and triple bottom line enterprises.

- Parallel approach: A range of investors and other stakeholders (for example, governments, nonprofit organizations, fishing collectives) develop coordinated investments to improve fisheries data, management, infrastructure, and triple bottom line enterprises. Efforts can be separately funded, but they work in tandem and share the ultimate goal of achieving sustainable catch with an appropriately capitalized and profitable fishing sector.

Each of these sequencing models presents particular challenges and opportunities. Structuring investments to achieve triple bottom line outcomes is still a new idea within the fisheries sector. There is growing evidence from other sectors, however, including agriculture and forestry, that these types of investments are achievable. Examples include the Moringa Fund[1] and Livelihood Funds,[2] which bring together public institutions, private investors, and NGOs, using innovative investment models to simultaneously address environmental degradation, climate change, and rural poverty while helping businesses become more sustainable.

The Impetus

Attracting impact investments is critical for the future of fishery recovery and expansion—these projects cannot rely on short-term loans and grants; they need longer-term finance that is committed to sustainability and responsibility. Development organizations, NGOs, and other noncommercial actors have a critical and catalytic role to play in crowding-in impact investment for sustainable fisheries by sharing risk with the private sector, promoting policy reforms, and funding interventions (through either concessional lending, grants, and/or technical assistance) with the intention of removing the barriers to impact investment.

Read the paper: Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries

[1] The Moringa Fund is a EUR 84 million investment fund that targets profitable large-scale agroforestry projects with high environmental and social impact in Latin America and Sub-Saharan Africa. The fund makes equity investments of EUR 4–10 million per project and adds value through its technical skills, environmental and social expertise, and global network.

[2] The Livelihood Funds are a series of investment funds created by Danone, which brings together investors—including Schneider Electric, Crédit Agricole S. A., Michelin, Hermès, SAP, CDC Climat, La Poste, Firmenich, and Voyageurs du Monde—to invest over EUR 40 million to finance nine on-the-ground programs for mangrove restoration, agroforestry, and rural energy.

-

Lead Firm Strategy Implementation – Indonesian Blue Swimming Crab

Overview

In 2015, Wilderness Markets completed a value chain summary of the blue swimming crab (BSC) fishery in Indonesia in which we analyzed the current state of fishery data systems, resource management, infrastructure, and enterprise capacity. Based on these findings, we recommend a lead firm strategy to move the fishery toward sustainability. Like many fisheries in emerging markets, the Indonesian BSC fishery lacks reliable data and, despite new national policies, functions largely without effective management. The value chain has strong, established commercial and social relationships, indicative of the power and influence of a small group of 16 processors buying from 400 mini-plants that, in turn, purchase crab from more than 65,000 fishermen.

In this case, the lead firm is a U.S. based company, Blue Star Foods. Blue Star is working to create financial and social incentives to enable fishermen to transition faster to sustainable fishing practices. Through its purchasing power and relationships, Blue Star is therefore in strong position to influence the practices of a range of processors, who have commercial relationships with a network of mini-plants, collectors, and fishermen.

Sumatran vessel with collapsible traps Lead Firm Pilot Design

With Blue Star and local harvesters, we are developing an investment model based on a pilot partnership between the lead firm and a fishing cooperative (in development). The model brings together philanthropic and private capital and provides financial, social, and environmental returns. It includes:

- Purchase commitments based on price, quality and standards

- Investments in fishermen cooperatives to motivate gear improvements

- Improved fishery data collection and traceability

- Support for harvest control compliance

This pilot is designed to attract private, return-seeking impact investment and complement ongoing work by NGOs to improve fishery management. We expect this approach will enable local fishermen to adopt sustainable practices faster than waiting for the government to independently create and enforce management changes, and without the economic hardship for fishermen that often accompanies changes in fishery regulations. It will also bolster business advocacy for more effective fisheries management policies and enforcement through a local cooperative structure.

BSC fisherman with new vessel tracking device Goals and expected outcomes

Ultimately, as a result of better data collection and effective management, the fishery will produce higher yields of BSC. It will also provide a traceable, sustainably harvested product with a competitive advantage in key U.S. and E.U. markets. This will then allow Blue Star and supporting investors to recoup their investments in sustainable practices.

By embedding this lead firm work within existing value chain relationships and practices, we aim to:

- Demonstrate the financial viability of investments in fishery data collection and management, thus attracting additional private investment in these practices.

- Create new norms that are sustained because of their business value and not ongoing philanthropic support or government subsidies.

- Provide clear and reliable financial benefits for small-scale fishermen to make gear changes; follow harvest control measures; and take on other sustainable fishing practices. Immediate economic well-being is thereby aligned with sustainable practices to improve compliance and reduce the localized short-term, negative impacts of fishery restrictions.

- Finally, test a new, “parallel” investment model for combining philanthropic, government, and private sector funding to address fishery management. If successful, other emerging market fisheries can tailor the model.

We are currently seeking additional partners to join us in this lead firm pilot project. Please get in touch with us if you would like more information and/or would like to get involved.

-

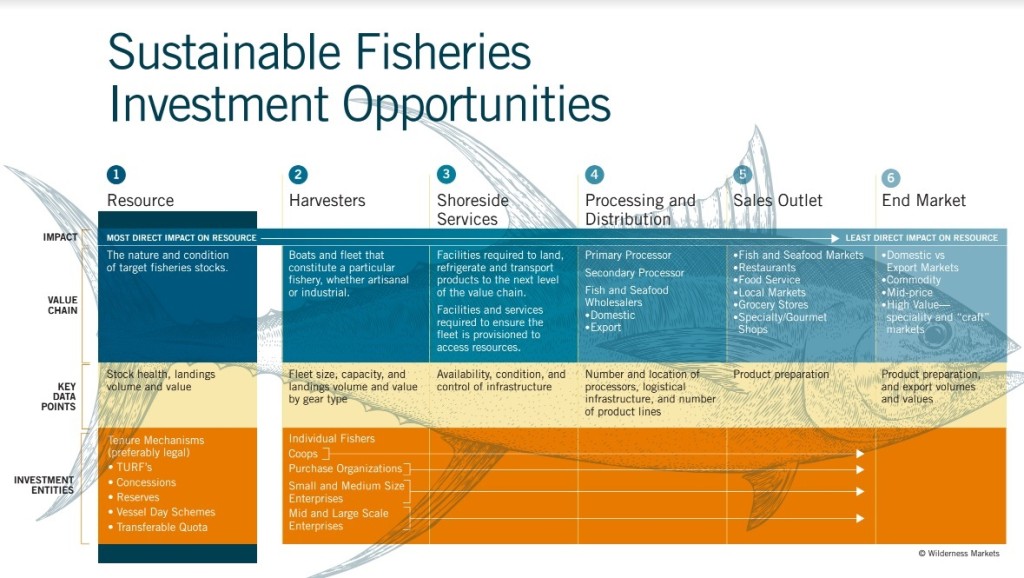

Current Paths for Sustainable Fisheries Investment

lnvestors, including impact investors, can invest in the fisheries sector through two general approaches (see figure below). The first, more traditional, approach invests in fishing or seafood supply chain businesses. Examples at the level of fishers in supply chain include funding for fishing companies or cooperatives to purchase more sustainable fishing gear (e.g., that excludes bycatch or protects ocean habitats), improve vessels, or buy cold storage equipment. Further up the supply chain are investments in processing and logistics businesses. Return on these investments stems from increased productivity and efficiency of fishing; reduced waste; increased access to markets; ; and/or higher product values.

The second approach for investors is at the resource level. For example, in some fisheries like West Coast Groundfish in the United States, investors can purchase rights to fish with the potential to sell or lease these rights for environmental, social, and/or financial benefit in the future. Similar to purchasing equity or stock in a company, equity in the right to fish in a limited-access fishery can be bought and sold. Examples include tradable fishing licenses, effort quota (such as vessel days), and fishing quota. Return on these investments relies on fish populations maintaining or increasing in abundance in the future.

These resource-level investments in the second approach require legally enforceable rights and robust tenure systems. As such, they currently exist almost exclusively in developed country fisheries that have robust ocean policies and strong legal systems to create, manage, and enforce ownership and transfer of fishing rights. Few of these resource-level investment opportunities exist in developing country fisheries.

Because of the open access nature of fisheries, without fisheries policy and management in place, investments in the supply chain are unlikely, in and of themselves, to improve the health of a fishery. They may reduce the impact of a participating firm or entity, but unless all firms apply the same standard, negative practices will continue to impede the recovery of a fishery.

More impactful are well structured resource level investments intrinsically tied to the biological recovery of a fishery. Improved fishery health will likely benefit these investments and thus drive a virtuous circle of fishery improvements, leading to improved social and economic outcomes, which in turn increases the economic value of the fishery.

Adapted from: Inamdar, Neel, Larry Band, Miguel Jorge, and Jada Tullos Anderson. Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries. Edited by Ashley Simons. Washington, D.C.: World Bank Group, 2016.

-

What lessons can be learned from the Icelandic cod value chain?

![Iceland - Siglufirði Siglufjörður By Hansueli Krapf This file was uploaded with Commonist. [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons](https://upload.wikimedia.org/wikipedia/commons/4/4b/2014-04-29_11-04-49_Iceland_-_Siglufir%C3%B0i_Siglufj%C3%B6r%C3%B0ur.JPG)

Iceland – Siglufirði Siglufjörður By Hansueli Krapf This file was uploaded with Commonist. [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons

Icelandic cod first came to our attention at Wilderness Markets when we were collaborating with Future of Fish on research into financing needs in the US Northeast Multispecies Sector Program. How can cod from, Iceland, over 2000 miles away be not only cheaper but of equal or better quality than cod caught from just outside your proverbial front door?

A series of papers highlights important developments and key factors in the success of the Icelandic cod value chain since the ‘90s. The series include:

- The Effects of Fisheries Management on the Icelandic Demersal Fish Value Chain, 2016[1]

- A Comparison of the Icelandic Cod Value Chain and the Yellow Fin Tuna Value Chain of Sri Lanka, 2010[2]

- The Role of Fish Markets in the Icelandic Value Chain of Cod, 2010[3]

- The Importance of SMEs in the Icelandic Fisheries Global Value Chain, July 2009[4]

- Structural Changes in the Icelandic Fisheries Sector – A Value Chain Analysis, 2008[5]

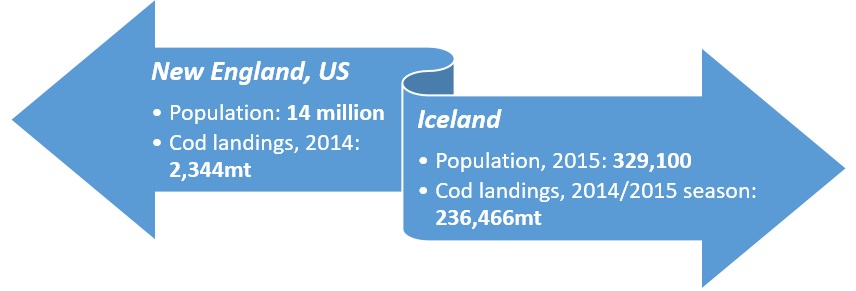

Before digging in too far, two aspects of the Icelandic versus the New England value chains can’t be overlooked—the relatively small population of Iceland and the relatively high landings of cod. For disputed reasons (climate change, better management, etc.) Iceland has a much healthier, i.e. more abundant stock, and hundred-fold greater landings than New England. Along with much higher landings, a far lower population means a robust export market.

Key factors and developments:

- Increased efficiency at multiple levels of the value chain has helped improve value

- Domestic value creation, specifically in the form of fresh fillets, has added significant value

- Information flow (availability of information) and knowledge drive value

- Use of marketing information to govern the value chain through vertical integrated companies and fish auction markets

- Fish markets (auctions) improve efficiency and improve the consistency of supply for the value chain by acting as clearinghouses and support speculation

- Consolidation of vessels, fishermen, processors, processing workers, and quota ownership have occurred in significant number

- Increased specializations in fishing and processing

An interesting aspect that warranted a whole paper is the role of the fish markets, effectively online auctions, wherein all bidding is done through one computerized system owned by 15 independent markets since 2000. These private markets only handle 20% of the landings by volume but have a high value in terms of value chain efficiency because they allow for specialization (buyers can sell or swap species not needed for production), provide stability (buyers can ‘top-up’ if they are short on supply) and creates market-driven value for species. The rise in general groundfish prices by 20% from 1999 to 2008 is thought to be partially attributed to the fish market system.

Some key aspects of the Icelandic cod value chain, like low human population in Iceland and abundance of target species in their waters, don’t readily translate to Wilderness Markets’ recent focus on the Indonesian and U.S. West Coast fisheries. Others do. For instance, in the paper on the importance of small and medium enterprises (SMEs), the increase in vertically integrated companies means those companies have better control of the reliability, quality and delivery of fisheries products. Their competitive advantages are related to quality assurance knowledge, good logistics and dedicated export and sales management. On an almost reverse timeline for the U.S. West Coast groundfish fishery in California, fish handling in Iceland improved in the ‘90s and ‘00s by investments in better onboard cooling systems, shorter fishing trips and logistics improvements.

In the 2016 paper, they also describe the structure of the value chain before the export licensing system was abolished in the 1980s—importantly, and with implications for other value chains – the three large marketing and sales organizations that controlled most of the fish failed to send market signals back to producers. The new, vertically integrated companies that replaced these organizations heeded signals from foreign customers and improved product quality and successfully added value domestically by switching processing to Iceland instead of overseas.

We have witnessed this same disconnect in many other fisheries; fishermen don’t seem to have any idea about the needs and demands of the end markets and have no incentive to meet these demands. In one of the most telling statements in the series, an interviewee states, “They [the Norwegians] are still mostly thinking about catching while we have reached the point where we think about serving the market.” Most fishermen have not yet been able to reach this stage, hindering their ability to realize improved value for their work.

We’re hopeful that the end-market research currently underway in California will provide market data that can be turned into increased value for the harvesters working diligently to promote sustainability.

[1] Knútsson, Ö., Kristófersson, D. M., & Gestsson, H. (2016). The effects of fisheries management on the Icelandic demersal fish value chain. Marine Policy, 63, 172-179..

[2] Knútsson, Ö., Gestsson, H., Klemensson, O., Thordarson, G., & Amaralal, L. (2010). A Comparison of the Icelandic Cod Value Chain and the Yellow Fin Tuna Value Chain in Sri Lanka.

[3] Knútsson, Ö., Klemensson, Ó., & Gestsson, H. (2010). The Role of Fish-Markets in the Icelandic Value Chain of Cod.

[4] Knútsson, Ö., Gestsson, H., & Klemensson, Ó. (2009, July). The importance of SMEs in the Icelandic fisheries global value chain. In IXX EAFE Conference Proceedings (pp. 6-9).

[5] Knútsson, Ö., Klemensson, Ó., & Gestsson, H. (2008). Structural changes in the Icelandic fisheries sector-a value chain analysis.

[6] New England Population: http://www.dlt.ri.gov/lmi/census/pop/neweng.htm

Iceland Population: http://www.iceland.is/the-big-picture/quick-factsUS landings: http://www.st.nmfs.noaa.gov/commercial-fisheries/commercial-landings/annual-landings/index

Icelandic landings: http://icefishnews.com/wp-content/uploads/2013/05/Marko-partners-%C3%ADslenski-kv%C3%B3tinn.png

{kind=link}