Impact investors are ready to invest increasing amounts of impact capital in sustainable fisheries; what’s missing are profitable businesses and organizations with the capacity to accept investment. These profitable “investible entities” aren’t emerging apace because the entrepreneurial ecosystem to develop their business capacity is lagging.

Tag: impact investing

-

Marine Heat Waves More Common and Lasting Longer Globally

A study done by the Marine Heatwaves International Working Group showed that there has been a 54% increase globally in the number of “marine heat wave days” per year since 1925.[1] Published in the Nature Communications journal and cited in News Deeply recently[2], the study cited the warm zone off the Western Australian coast in 2011 and the Gulf of Maine episode in 2012 as incidences of this trend. Average ocean temperatures have been increasing but these marine heat waves are also increasing in frequency and duration. The combination of the two are linked to factors that damage ecosystems and economies.

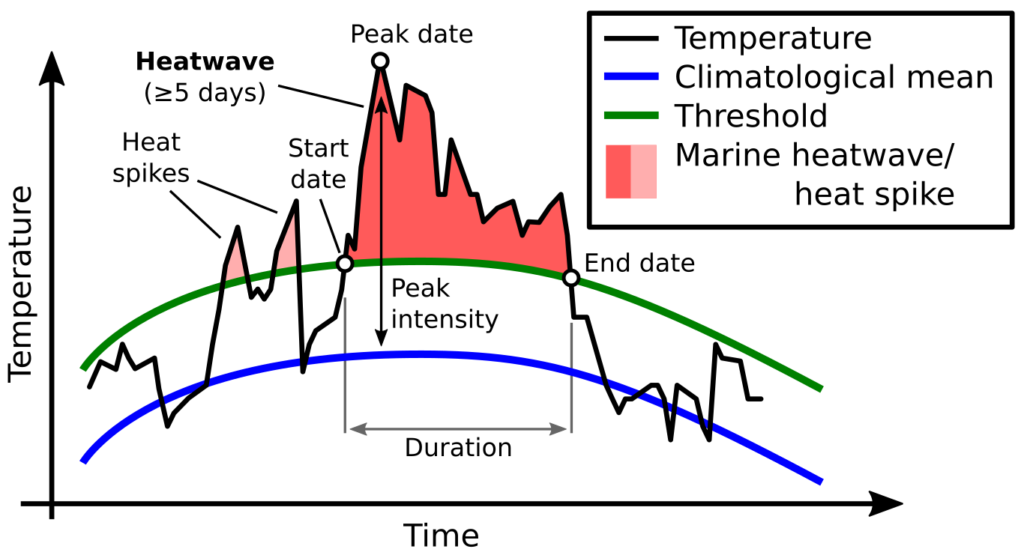

Figure 1 Graphic explanation of Marine Heat Waves, from http://www.marineheatwaves.org/all-about-mhws.html

Marine heat waves (MHWs) are “…prolonged periods of anomalously high sea surface temperatures… [that] have had severe impacts on marine ecosystems in recent years.” (Oliver et al., 2018). In Australia alone, Shark Bay in Western Australia lost 36% of its seagrass meadows and carbon storage, and the Great Barrier Reef suffered four mass coral bleaching events because of these extended periods of elevated sea surface temperatures.[3]

There are significant ecological and economic effects arising from these marine heat waves. They include:

“… sustained loss of kelp forests, coral bleaching, reduced surface chlorophyll levels due to increased surface layer stratification, mass mortality of marine invertebrates due to heat stress, rapid long-distance species’ range shifts and associated reshaping of community structure, fishery closures or quota changes and even intensified economic tensions between nations.” (Oliver et al., 2018)[4]

According to Eric Oliver, the study’s lead author, “…in the early 20th century, there was an average of two marine heat waves per year globally, but now there are three or four. While they used to last 10 days on average, they now last for an average of 13 or 14 days.”[5]

The study suggests that marine heat waves will continue to increase with the ongoing global warming.

Why does Wilderness Markets care about anemones and anemonefish? Because our work requires us to look not only at enterprises and fishery management, but at the entire ecosystem to properly account for business risks. Learn more about us.

[1] Oliver, E. C. J et al. (2018). Longer and more frequent marine heatwaves over the past century. Nature Communications, 9. doi: 10.1038/s41467-018-03732-9

[2] News Deeply. (2018). Executive Summary for April 13th. Oceans Deeply (Marine Heatwaves Are Longer, More Frequent). Retrieved from https://www.newsdeeply.com/oceans/executive-summaries/2018/04/13.

[3] McSweeney, R. (2018). Marine heatwaves have become ‘34% more likely’ over past century. Carbon Brief. Marine heatwaves have become ‘34% more likely’ over past century. Retrieved from https://www.carbonbrief.org/marine-heatwaves-have-become-34-more-likely-over-past-century.

[4] Oliver, E. C. J et al.

[5] Willick, F. (2018). Ocean heat waves becoming more common, longer, new study finds. CBC. Retrieved from http://www.cbc.ca/news/canada/nova-scotia/marine-heat-wave-ocean-hot-spot-study-1.4611794

-

West Coast Pilot – Culinary Workshop

A previous post outlined our pilot project in California with Changing Tastes; this post provides a peek into a culinary workshop that is part of the planning phase.

Purpose

As part of our work to reintroduce local fish back into local markets in California, our foremost consideration is how to reintroduce them to our plates and palates. Without delicious dishes and high quality products, winning back a space on the plate will be impossible.

To discover how local fish can create a winning combination of flavor, presentation, and affordability for chefs in corporate dining, our partner Changing Tastes arranged a culinary workshop in California. More than a dozen chefs and several sustainability managers from the same or similar groups joined us in mid-November at a test kitchen in the Bay Area to develop the recipes and messaging needed to successfully bring back Californian West Coast Groundfish.

Palate and Pocket

To explore which fish could please both palates and pocketbooks, the chefs spent the morning preparing a sampling of locally-caught fish, including Dover and petrale sole, boccaccio, chilipepper and black gill rockfish, and sablefish (AKA black cod) provided by Real Good Fish. These fish represent the spectrum of species that are part of the West Coast Groundfish program, one of the most sustainably managed fisheries in the world, and one that has the fish to prove the stocks are healthy. These are fairly common landings that span from very inexpensive Dover to higher-end sablefish. The variety of textures, thicknesses and tastes were highlighted in Latin and Asian-inspired themes, such as black gill fish tacos with mango slaw (Chef Ochoa), petrale-coconut ceviche (Chef Fogata), black and white coconut crusted black cod (Chef Thomas), and steamed Szechuan boccaccio (Chef Hernaez).

Heart and Mind

Equally important to taste and cost is persuading diners to try these new dishes. In a nearby space, restaurant industry marketing and communications executives as well as sustainability managers and representatives of groups that support sustainable seafood brainstormed marketing ideas for the dining spaces where the fish will be offered to diners next spring.

Common themes included emphasizing that the fish is locally-caught in California. They noted that “local” often implies fresh to diners. Including a map of the different ports where the fish originates from for the pilot, and identifying fishermen and women from each was another popular theme.

Marketing experts, chefs, sustainability managers and others agree on not using the word “groundfish” in marketing materials. This group and others realize that this collective term for these species isn’t one that necessarily appeals to diners, nor does it help them understand the diversity of species and flavors within the broad category.

Pilot Evaluation

Among potential evaluation methods and data points, our participants identified these as the most likely:

- On-site, established food focus groups

- Measurement of orders by volume

- Gauging the relationship between price of dishes and purchases

- Comparison to sales of other seafood dishes

- Comment cards

- Online commenting system

- Surveys, potentially with incentives, and/or provided in a quick format via touchpad at the point of purchase

- Querying the culinary team during and after the pilot

Post-workshop steps

Our next tasks are confirming which specific dining halls and cafes will participate from each of the corporate dining partners and confirming likely order volume by species or species group, e.g., petrale sole is a species and rockfish is a species group. Almost simultaneously, we will work with the corporate dining partner and their existing distributors to determine the likely sources, feasible start dates, and volumes. We look forward to sharing updates as this work progresses in 2018.

-

How to Develop Impact Investment Opportunities in Sustainable Fisheries

The Need for Sustainable Fisheries Finance

We know all the problems associated with overfishing and we know that research shows:

1) that switching to more sustainable management will lead to increased revenues and food security; and

2) the cost for doing so exceeds what can be provided through traditional development and philanthropic organization.How do we get past the second to make the first possible? Supported by the World Bank, and with input from dozens of impact investors and fishery experts, we detail the main barriers and potential approaches to overcome them in our latest paper: Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries.

Who Should Read This Paper

This paper provides an overview for international development organizations, development finance institutions, NGOs, and the governments they work with of (i) the key concerns that impact investors may have when considering the financing of sustainable fisheries, and (ii) potential approaches for public-private partnerships to overcome these obstacles. It is intended as a primer for these actors, to understand the perspective of the commercial impact investor.

Overview

This paper explains the central challenges that keep impact investors from participating in sustainable fisheries, and is structured along four main barriers:

- A lack of reliable fishery data

- Ineffective fisheries management

- Unreliable infrastructure systems

- A paucity of investment-ready enterprises

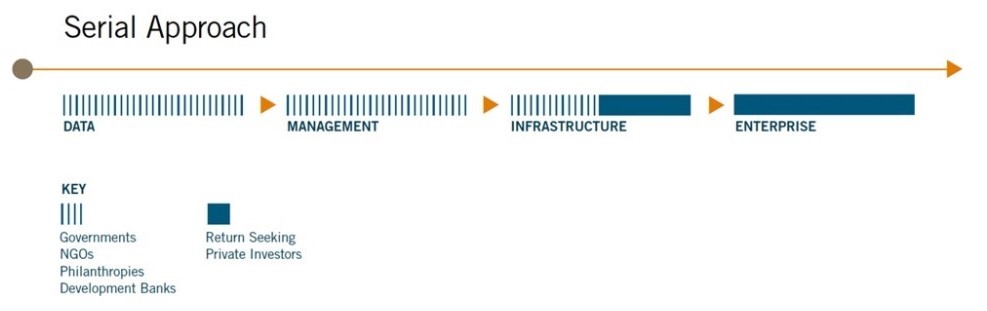

It then proposes three models for sequencing and combining different sources of capital to overcome these obstacles:

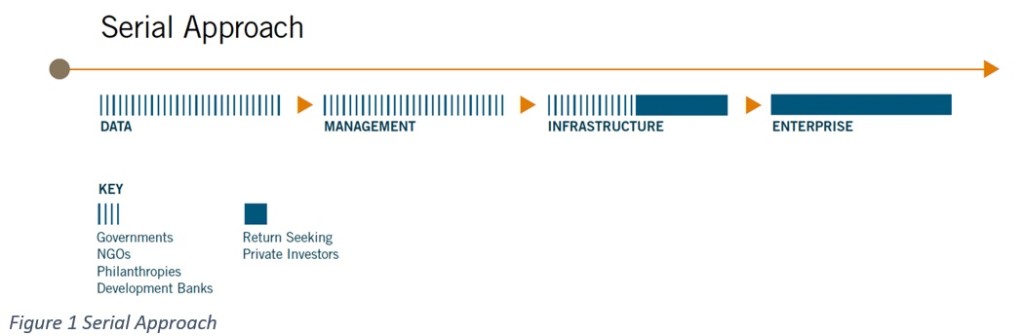

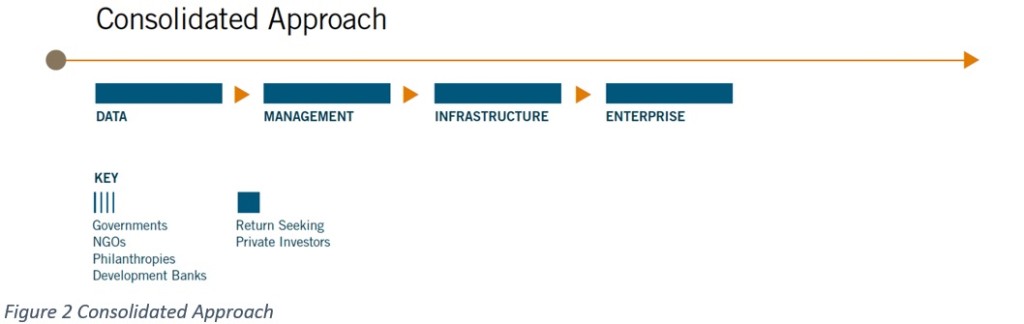

- Serial approach: Public and philanthropic funders first support the establishment of strong governance arrangements, improved data collection, and fishery management. Once these initiatives mitigate some of the risk associated with a fishery investment, then return-seeking investors are incentivized to finance sustainable infrastructure projects (often through public-private partnerships) and/or enterprises along the value chain, focused on outcomes that achieve a triple bottom line: social responsibility, economic value, and environmental impact.

- Consolidated approach: Governments negotiate agreements with a single private sector entity or cooperative to delegate fishery management responsibilities. The private firm or cooperative then simultaneously invests in fishery data, management, infrastructure, and triple bottom line enterprises.

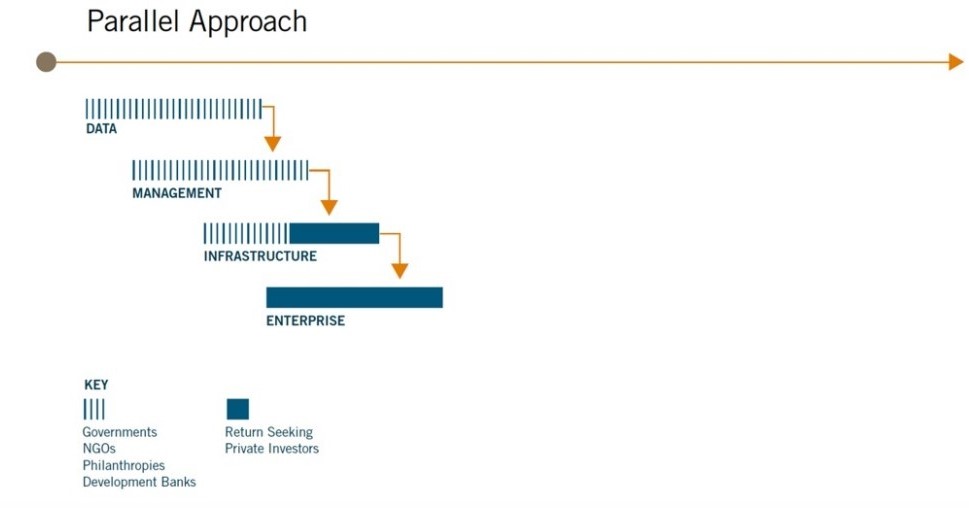

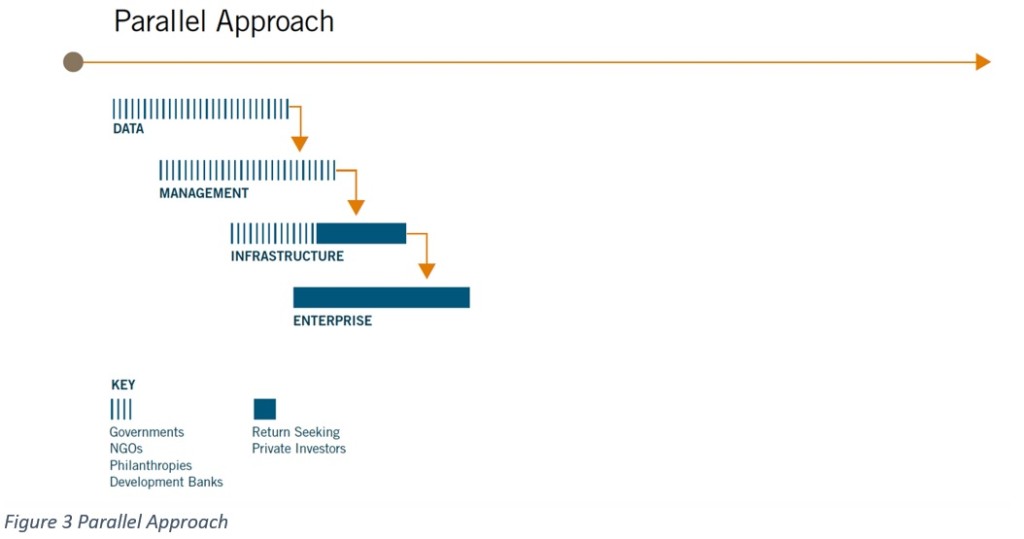

- Parallel approach: A range of investors and other stakeholders (for example, governments, nonprofit organizations, fishing collectives) develop coordinated investments to improve fisheries data, management, infrastructure, and triple bottom line enterprises. Efforts can be separately funded, but they work in tandem and share the ultimate goal of achieving sustainable catch with an appropriately capitalized and profitable fishing sector.

Each of these sequencing models presents particular challenges and opportunities. Structuring investments to achieve triple bottom line outcomes is still a new idea within the fisheries sector. There is growing evidence from other sectors, however, including agriculture and forestry, that these types of investments are achievable. Examples include the Moringa Fund[1] and Livelihood Funds,[2] which bring together public institutions, private investors, and NGOs, using innovative investment models to simultaneously address environmental degradation, climate change, and rural poverty while helping businesses become more sustainable.

The Impetus

Attracting impact investments is critical for the future of fishery recovery and expansion—these projects cannot rely on short-term loans and grants; they need longer-term finance that is committed to sustainability and responsibility. Development organizations, NGOs, and other noncommercial actors have a critical and catalytic role to play in crowding-in impact investment for sustainable fisheries by sharing risk with the private sector, promoting policy reforms, and funding interventions (through either concessional lending, grants, and/or technical assistance) with the intention of removing the barriers to impact investment.

Read the paper: Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries

[1] The Moringa Fund is a EUR 84 million investment fund that targets profitable large-scale agroforestry projects with high environmental and social impact in Latin America and Sub-Saharan Africa. The fund makes equity investments of EUR 4–10 million per project and adds value through its technical skills, environmental and social expertise, and global network.

[2] The Livelihood Funds are a series of investment funds created by Danone, which brings together investors—including Schneider Electric, Crédit Agricole S. A., Michelin, Hermès, SAP, CDC Climat, La Poste, Firmenich, and Voyageurs du Monde—to invest over EUR 40 million to finance nine on-the-ground programs for mangrove restoration, agroforestry, and rural energy.

-

Governance or a Markets Approach? Both. Adopt a Parallel Approach to Fisheries Reform

In our previous posts, we’ve discussed reasons and ways for involving private capital in fisheries reform, including taking a lead firm approach. This post about the parallel approach is a direct follow-up to the three models we propose for investment sequencing; we recommend checking out that post first.

Overview

Is there only one way to make a fishery sustainable? We don’t think so. That said, we do know that there are some key areas that need support on the way to sustainability. Indeed, whether to consider a “governance” or “markets” approach to fishery sustainability is a false dichotomy. In areas where a market is present, which is most, governance and markets must be considered simultaneously and balanced for the short and long-term benefits.

The working model we’re developing adopts a parallel approach to address the challenges associated with developing countries fishery reform. In this approach, the markets, and by definition, the private sector, are key partners. The commercial relationships with harvesters developed by this model are critical to ensuring support for long term fisheries reform given the lack of representation and organization at the base of the value chain. We explain our thinking in more detail below.

Approaches to Management

Under ideal circumstances, fisheries reform would have a “serial” approach to design, implement, and enforce regulations. Scientific and economic data would be the bases for robust fisheries management. With reasonable assurance that stocks will not be overfished, value chain participants can plan investments in tandem with stock recoveries.

Emerging market fisheries face significant social and political concerns to the serial approach. For example, legislating changes that result in reduced fishing effort to promote species and stock recovery has political and social ramifications that not all governments are prepared to address. Furthermore, the cost of enforcing such changes are likely to be higher than what is considered normal – both in monetary and social terms.

Given the desire to reform fisheries while also demonstrating the economic benefits associated with such reform, we propose that a “parallel” approach may be more appropriate in emerging markets. In this approach, different actors work in tandem to develop and implement measures to increase sustainability.

What’s are the Management Basics?

Investments to improve data and management are primary concerns for fisheries reform as these will demonstrate the success and costs of various efforts. Though species, geographies and cultural norms vary, there are some agreed-upon fishery management principals which will be informed and supported by good data. These include five parameters for:

- size,

- sex,

- seasons,

- geographies and

- ability to access to the fishery.

Generally, social and legal changes necessary to create and enforce these management measures increase as complexity and distance from the resource increases. The degree to which the value chain can enforce them runs in the opposite direction. That is, the value chain has the greatest potential to enforce size, sex and seasons, but their ability to enforce rules decreases for geographic restrictions and even more so for access control. Rulemaking must involve local society and governments, and their participation is particularly important for complex tasks like access and geography restrictions.

The blue swimming crab (BSC) fishery in Indonesia is a good example of a parallel approach opportunity that currently engages both the value chain and government. National government has already adopted and passed restrictions regarding size and sex. The challenge now is how best to implement and enforce these efforts.

Working Model

In our parallel approach model, value chain stakeholders in Indonesia have begun gathering data to help inform and reinforce decision-making. At the same time, the provincial government, in cooperation and communication with the local community, will set standards and provide enforcement for the five parameters. Managing seasonality, geographic limits and access restrictions are also actionable through the value chain. However, these will require a higher degree of social acceptance, enforcement and value chain adoption. Good data from working closely with cooperatives and harvesters will provide foundation for the harvest control strategies. We envision starting with the easiest strategies first, essentially moving from 1 (size) down to 5 (access control) over a period of less than four years for creation and testing of the rules. It is imperative that the local government and community create the standards to ensure the lead firm can work to establish sustainability within the fishery.

The value chain and lead firm approaches provide a valuable opportunity to implement effective enforcement needed to achieve sustainability. Value chain participants can insist on the adoption of these standards, which may then be verified based on effective data collection and using internal and external audits. The current working model also includes a proposal for the lead firm to make purchases through a preferred supplier network currently formed as a cooperative. Consequently, access to finance for value chain stakeholders will be contingent upon their compliance with the rules. Working in collaboration with local cooperatives and harvesters, the economics of this fishery are such that all participants should benefit from improved BSC size and abundance.

Final Thoughts on the Parallel Approach

Ideally, government would provide the necessary framework and policies to implement these strategies, while providing effective enforcement as in the serial approach to reform. However, in the absence of this involvement, providing market-based opportunities to adopt these measures in a socially acceptable manner may provide a viable alternative approach, which is why the parallel approach is the most viable in many fisheries like BSC in Indonesia.

-

Lead Firm Strategy Implementation – Indonesian Blue Swimming Crab

Overview

In 2015, Wilderness Markets completed a value chain summary of the blue swimming crab (BSC) fishery in Indonesia in which we analyzed the current state of fishery data systems, resource management, infrastructure, and enterprise capacity. Based on these findings, we recommend a lead firm strategy to move the fishery toward sustainability. Like many fisheries in emerging markets, the Indonesian BSC fishery lacks reliable data and, despite new national policies, functions largely without effective management. The value chain has strong, established commercial and social relationships, indicative of the power and influence of a small group of 16 processors buying from 400 mini-plants that, in turn, purchase crab from more than 65,000 fishermen.

In this case, the lead firm is a U.S. based company, Blue Star Foods. Blue Star is working to create financial and social incentives to enable fishermen to transition faster to sustainable fishing practices. Through its purchasing power and relationships, Blue Star is therefore in strong position to influence the practices of a range of processors, who have commercial relationships with a network of mini-plants, collectors, and fishermen.

Sumatran vessel with collapsible traps Lead Firm Pilot Design

With Blue Star and local harvesters, we are developing an investment model based on a pilot partnership between the lead firm and a fishing cooperative (in development). The model brings together philanthropic and private capital and provides financial, social, and environmental returns. It includes:

- Purchase commitments based on price, quality and standards

- Investments in fishermen cooperatives to motivate gear improvements

- Improved fishery data collection and traceability

- Support for harvest control compliance

This pilot is designed to attract private, return-seeking impact investment and complement ongoing work by NGOs to improve fishery management. We expect this approach will enable local fishermen to adopt sustainable practices faster than waiting for the government to independently create and enforce management changes, and without the economic hardship for fishermen that often accompanies changes in fishery regulations. It will also bolster business advocacy for more effective fisheries management policies and enforcement through a local cooperative structure.

BSC fisherman with new vessel tracking device Goals and expected outcomes

Ultimately, as a result of better data collection and effective management, the fishery will produce higher yields of BSC. It will also provide a traceable, sustainably harvested product with a competitive advantage in key U.S. and E.U. markets. This will then allow Blue Star and supporting investors to recoup their investments in sustainable practices.

By embedding this lead firm work within existing value chain relationships and practices, we aim to:

- Demonstrate the financial viability of investments in fishery data collection and management, thus attracting additional private investment in these practices.

- Create new norms that are sustained because of their business value and not ongoing philanthropic support or government subsidies.

- Provide clear and reliable financial benefits for small-scale fishermen to make gear changes; follow harvest control measures; and take on other sustainable fishing practices. Immediate economic well-being is thereby aligned with sustainable practices to improve compliance and reduce the localized short-term, negative impacts of fishery restrictions.

- Finally, test a new, “parallel” investment model for combining philanthropic, government, and private sector funding to address fishery management. If successful, other emerging market fisheries can tailor the model.

We are currently seeking additional partners to join us in this lead firm pilot project. Please get in touch with us if you would like more information and/or would like to get involved.

-

Current Paths for Sustainable Fisheries Investment

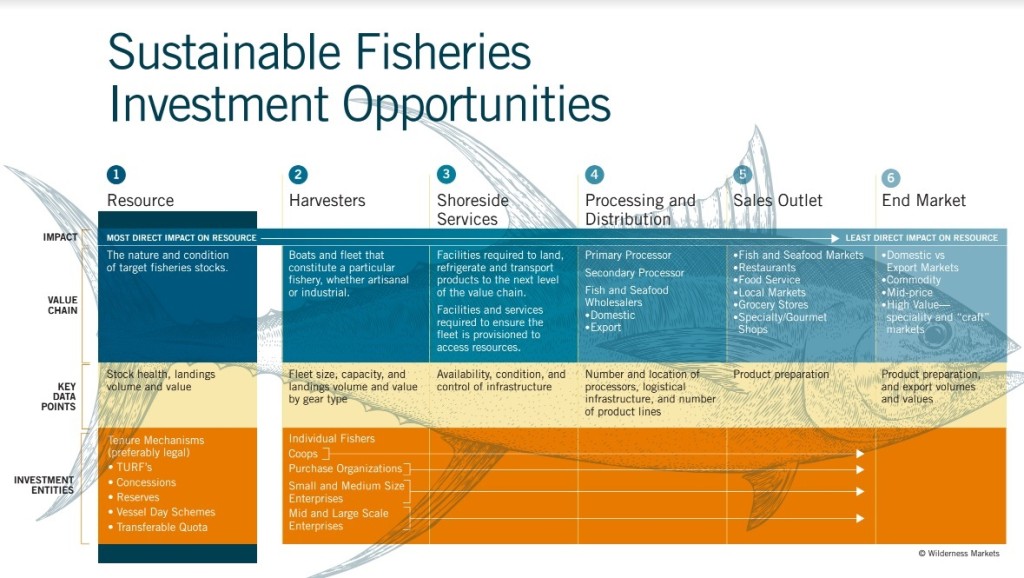

lnvestors, including impact investors, can invest in the fisheries sector through two general approaches (see figure below). The first, more traditional, approach invests in fishing or seafood supply chain businesses. Examples at the level of fishers in supply chain include funding for fishing companies or cooperatives to purchase more sustainable fishing gear (e.g., that excludes bycatch or protects ocean habitats), improve vessels, or buy cold storage equipment. Further up the supply chain are investments in processing and logistics businesses. Return on these investments stems from increased productivity and efficiency of fishing; reduced waste; increased access to markets; ; and/or higher product values.

The second approach for investors is at the resource level. For example, in some fisheries like West Coast Groundfish in the United States, investors can purchase rights to fish with the potential to sell or lease these rights for environmental, social, and/or financial benefit in the future. Similar to purchasing equity or stock in a company, equity in the right to fish in a limited-access fishery can be bought and sold. Examples include tradable fishing licenses, effort quota (such as vessel days), and fishing quota. Return on these investments relies on fish populations maintaining or increasing in abundance in the future.

These resource-level investments in the second approach require legally enforceable rights and robust tenure systems. As such, they currently exist almost exclusively in developed country fisheries that have robust ocean policies and strong legal systems to create, manage, and enforce ownership and transfer of fishing rights. Few of these resource-level investment opportunities exist in developing country fisheries.

Because of the open access nature of fisheries, without fisheries policy and management in place, investments in the supply chain are unlikely, in and of themselves, to improve the health of a fishery. They may reduce the impact of a participating firm or entity, but unless all firms apply the same standard, negative practices will continue to impede the recovery of a fishery.

More impactful are well structured resource level investments intrinsically tied to the biological recovery of a fishery. Improved fishery health will likely benefit these investments and thus drive a virtuous circle of fishery improvements, leading to improved social and economic outcomes, which in turn increases the economic value of the fishery.

Adapted from: Inamdar, Neel, Larry Band, Miguel Jorge, and Jada Tullos Anderson. Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries. Edited by Ashley Simons. Washington, D.C.: World Bank Group, 2016.

-

Developing investment opportunities in sustainable marine capture fisheries

Marine fisheries provide an important source of food and livelihoods for millions of people globally, contributing more than US $274 billion to the global economy[1] and some estimates of the potential net gain for improved management at US $600-$1400 billion in present value over fifty years after rebuilding fish stocks[2].

How can governments, development banks, philanthropic grant-makers, and nonprofit organizations create the conditions that will attract and recruit impact investors to participate in the sustainable fisheries sector and contribute to the long-term value of global fisheries? We at Wilderness Markets recently tackled this question as part of our work with World Bank.

The first step is to clearly understand the barriers that keep these investors from engaging with sustainable fisheries and the information they need to evaluate investments. With this knowledge in hand, leaders in government, international development, and philanthropy can align their own funding to create the conditions for more capital to contribute to sustainable fisheries.

The central challenges that keep return-seeking investors from participating in sustainable fisheries fall into four main categories: a lack of fishery data, ineffective fisheries management, unreliable infrastructure systems, and a paucity of investment-ready opportunities.

We propose three potential models for sequencing and combining different sources of capital to overcome these obstacles and achieve sustainable fisheries:

- Serial Approach: Public and philanthropic funders first support the establishment of strong governance, data collection, and management of a fishery. Based on the de-risking effort of these initial projects, return-seeking investors subsequently fund sustainable infrastructure projects (often in conjunction with public resources) and/or enterprises focused on triple bottom line outcomes.

- Consolidated Approach: Governments negotiate agreements with a single private sector entity or cooperative to delegate fishery management responsibilities. The private firm or cooperative then simultaneously invests in fishery data, management, infrastructure, and triple bottom-line enterprises.

- Parallel Approach: A range of investors and other stakeholders (e.g., governments, nonprofit organizations, fishing collectives) develop concurrent and coordinated investments in fisheries data, management, infrastructure, and triple bottom line enterprises. Each effort is separately funded, but they work in tandem and share the ultimate goal of achieving sustainable catch with an appropriately capitalized and profitable fishing sector.

Each of the above sequencing models has pros and cons, and each warrants additional exploration; making return-seeking investments that achieve the triple bottom line outcomes of social, environmental, and economic benefits is early on in it its evolution within the fisheries sector. They hold potential to attract additional funds and encourage private-sector approaches to help speed the transition to sustainable fisheries.

Adapted from: Inamdar, Neel, Larry Band, Miguel Jorge, and Jada Tullos Anderson. Developing Impact Investment Opportunities for Return-Seeking Capital in Sustainable Marine Capture Fisheries. Edited by Ashley Simons. Washington, D.C.: World Bank Group, 2016.

[1] World Bank. 2012. “Hidden Harvest: The Global Contribution of Capture Fisheries.” 66469–GLB. https://openknowledge.worldbank.org/bitstream/handle/10986/11873/664690ESW0P1210120HiddenHarvest0web.pdf?sequence=1

[2] Sumaila, Ussif Rashid, William Cheung, Andrew Dyck, Kamal Gueye, Ling Huang, Vicky Lam, Daniel Pauly, et al. 2012. “Benefits of Rebuilding Global Marine Fisheries Outweigh Costs.” Edited by Julian Clifton. PLoS ONE 7 (7): e40542. doi:10.1371/journal.pone.0040542.

-

What does stock health tell us about potential investments?

What’s an easy way for an investor to tell if a natural resource-based enterprise is going to be viable in three to five years? Part of that answer lies in evaluating the business and the regulatory environments in which it operates, but for natural resources in particular, the resource base trend needs to be examined; is it predicted that there will be more or less in the future, based on current extraction rates and scientific estimates of the resource level? And for conservation-focused impact investments, how can investors ensure they are not using more than the ecosystem can sustain?

In wild-capture fisheries, this translates to: “Will there be more or less of the fish to harvest in the future? Will my investment exacerbate overfishing?” Less fish to harvest means the effort level, and thus costs, will need to increase to find the remaining fish.

We’ve recently been puzzling through the easiest way for banks and impact investors to gauge the investability of fisheries enterprises, with a focus on Indonesia. Indonesia hosts some of the most biodiverse ocean ecosystems on our planet and is the world’s second largest harvester of wild capture fish. Banks and investors need quick, easily understood data that doesn’t unnecessarily burden their due diligence process but ensures they aren’t contributing to overfishing.

One tool that is already available in many fisheries is the stock assessment status, usually indicated as under- or moderately exploited, fully exploited, or over-exploited. The exploitation levels reflect scientific data on whether the fish in a fishery (the stock) are being sustainably harvested. Fully exploited indicates a stock that is thought to be fished and reproducing at nearly equal rates, i.e., the amount of fish harvested is the same as the fish being hatched and surviving to maturity. Over-exploited means harvest rates are too high, and under-exploited means they could increase rates without having a harmful effect on stocks.

Indonesia’s Ministry of Marine Affairs and Fisheries recently released the results of the National Commission on Stock Assessments (NOMOR 47/KEPMEN-KP/2016 TENTANG). The assessment provides an updated snapshot of ministry data in each fishery management area for the status of nine Indonesian fishery stocks.

In addition to focusing government investments on improving the fishery health, we think the data can be useful for banks and investors. The assessment data can help investors quickly determine the potential health of the resource an enterprise relies on, helping to ensure they are not causing more fish to be used than can be replaced. The key to balancing conservation and investment entails finding new opportunities to do more, without using more.

Disclaimer

The findings and conclusions in this report represent the interpretations of Wilderness Markets and do not necessarily reflect the view of expert stakeholders. This publication has been prepared solely for informational purposes, and has been prepared in good faith on the basis of information available at the date of publication without any independent verification. Wilderness Markets does not guarantee or warrant the accuracy, reliability, adequacy, completeness or currency of the information in this publication nor its usefulness in achieving any purpose. Charts and graphs provided herein are for illustrative purposes only. Nothing contained herein constitutes investment, legal, tax, or other advice nor is it to be relied on in making an investment or other decision. Readers are responsible for assessing the relevance and accuracy of the content of this publication. this publication should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell securities or to adopt any investment strategy.

-

What lessons can be learned from the Icelandic cod value chain?

![Iceland - Siglufirði Siglufjörður By Hansueli Krapf This file was uploaded with Commonist. [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons](https://upload.wikimedia.org/wikipedia/commons/4/4b/2014-04-29_11-04-49_Iceland_-_Siglufir%C3%B0i_Siglufj%C3%B6r%C3%B0ur.JPG)

Iceland – Siglufirði Siglufjörður By Hansueli Krapf This file was uploaded with Commonist. [CC BY-SA 3.0 (http://creativecommons.org/licenses/by-sa/3.0)], via Wikimedia Commons

Icelandic cod first came to our attention at Wilderness Markets when we were collaborating with Future of Fish on research into financing needs in the US Northeast Multispecies Sector Program. How can cod from, Iceland, over 2000 miles away be not only cheaper but of equal or better quality than cod caught from just outside your proverbial front door?

A series of papers highlights important developments and key factors in the success of the Icelandic cod value chain since the ‘90s. The series include:

- The Effects of Fisheries Management on the Icelandic Demersal Fish Value Chain, 2016[1]

- A Comparison of the Icelandic Cod Value Chain and the Yellow Fin Tuna Value Chain of Sri Lanka, 2010[2]

- The Role of Fish Markets in the Icelandic Value Chain of Cod, 2010[3]

- The Importance of SMEs in the Icelandic Fisheries Global Value Chain, July 2009[4]

- Structural Changes in the Icelandic Fisheries Sector – A Value Chain Analysis, 2008[5]

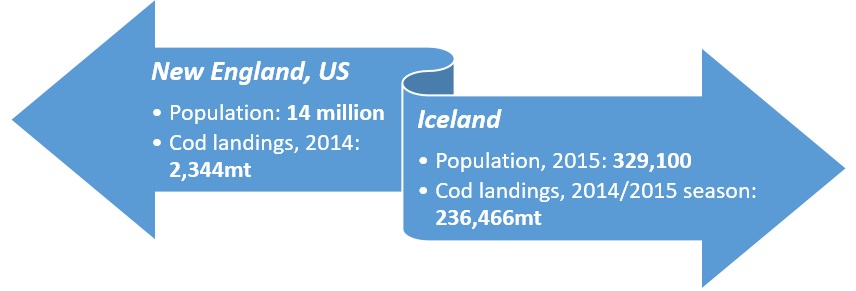

Before digging in too far, two aspects of the Icelandic versus the New England value chains can’t be overlooked—the relatively small population of Iceland and the relatively high landings of cod. For disputed reasons (climate change, better management, etc.) Iceland has a much healthier, i.e. more abundant stock, and hundred-fold greater landings than New England. Along with much higher landings, a far lower population means a robust export market.

Key factors and developments:

- Increased efficiency at multiple levels of the value chain has helped improve value

- Domestic value creation, specifically in the form of fresh fillets, has added significant value

- Information flow (availability of information) and knowledge drive value

- Use of marketing information to govern the value chain through vertical integrated companies and fish auction markets

- Fish markets (auctions) improve efficiency and improve the consistency of supply for the value chain by acting as clearinghouses and support speculation

- Consolidation of vessels, fishermen, processors, processing workers, and quota ownership have occurred in significant number

- Increased specializations in fishing and processing

An interesting aspect that warranted a whole paper is the role of the fish markets, effectively online auctions, wherein all bidding is done through one computerized system owned by 15 independent markets since 2000. These private markets only handle 20% of the landings by volume but have a high value in terms of value chain efficiency because they allow for specialization (buyers can sell or swap species not needed for production), provide stability (buyers can ‘top-up’ if they are short on supply) and creates market-driven value for species. The rise in general groundfish prices by 20% from 1999 to 2008 is thought to be partially attributed to the fish market system.

Some key aspects of the Icelandic cod value chain, like low human population in Iceland and abundance of target species in their waters, don’t readily translate to Wilderness Markets’ recent focus on the Indonesian and U.S. West Coast fisheries. Others do. For instance, in the paper on the importance of small and medium enterprises (SMEs), the increase in vertically integrated companies means those companies have better control of the reliability, quality and delivery of fisheries products. Their competitive advantages are related to quality assurance knowledge, good logistics and dedicated export and sales management. On an almost reverse timeline for the U.S. West Coast groundfish fishery in California, fish handling in Iceland improved in the ‘90s and ‘00s by investments in better onboard cooling systems, shorter fishing trips and logistics improvements.

In the 2016 paper, they also describe the structure of the value chain before the export licensing system was abolished in the 1980s—importantly, and with implications for other value chains – the three large marketing and sales organizations that controlled most of the fish failed to send market signals back to producers. The new, vertically integrated companies that replaced these organizations heeded signals from foreign customers and improved product quality and successfully added value domestically by switching processing to Iceland instead of overseas.

We have witnessed this same disconnect in many other fisheries; fishermen don’t seem to have any idea about the needs and demands of the end markets and have no incentive to meet these demands. In one of the most telling statements in the series, an interviewee states, “They [the Norwegians] are still mostly thinking about catching while we have reached the point where we think about serving the market.” Most fishermen have not yet been able to reach this stage, hindering their ability to realize improved value for their work.

We’re hopeful that the end-market research currently underway in California will provide market data that can be turned into increased value for the harvesters working diligently to promote sustainability.

[1] Knútsson, Ö., Kristófersson, D. M., & Gestsson, H. (2016). The effects of fisheries management on the Icelandic demersal fish value chain. Marine Policy, 63, 172-179..

[2] Knútsson, Ö., Gestsson, H., Klemensson, O., Thordarson, G., & Amaralal, L. (2010). A Comparison of the Icelandic Cod Value Chain and the Yellow Fin Tuna Value Chain in Sri Lanka.

[3] Knútsson, Ö., Klemensson, Ó., & Gestsson, H. (2010). The Role of Fish-Markets in the Icelandic Value Chain of Cod.

[4] Knútsson, Ö., Gestsson, H., & Klemensson, Ó. (2009, July). The importance of SMEs in the Icelandic fisheries global value chain. In IXX EAFE Conference Proceedings (pp. 6-9).

[5] Knútsson, Ö., Klemensson, Ó., & Gestsson, H. (2008). Structural changes in the Icelandic fisheries sector-a value chain analysis.

[6] New England Population: http://www.dlt.ri.gov/lmi/census/pop/neweng.htm

Iceland Population: http://www.iceland.is/the-big-picture/quick-factsUS landings: http://www.st.nmfs.noaa.gov/commercial-fisheries/commercial-landings/annual-landings/index

Icelandic landings: http://icefishnews.com/wp-content/uploads/2013/05/Marko-partners-%C3%ADslenski-kv%C3%B3tinn.png

{kind=link}